The Gold Report: The price of gold flirted with $1,300 per ounce ($1,300/oz) in January. In July, it fell below $1,100/oz. What happened?

Joe Mazumdar: Gold began 2015 at $1,184/oz. So, year to date it's down about 8% in U.S. dollars. And one of the primary reasons for that is the strength of the U.S. dollar, underpinned by an economic rebound and the anticipation of an interest rate hike in the latter part of 2015. From January to July 2015, the U.S. dollar as proxied by the trade-weighted index, the U.S. Dollar Index (DXY), was up by the same amount as the U.S. dollar-denominated gold price was down, 8%.

Source: Bloomberg

Source: Bloomberg

Gold's sideways to downward trend is underpinned by weak demand fundamentals. Overall Q1/15 demand—1,079.4 tonnes—as provided by the World Gold Council, was in line with the last two-year quarterly average. However, jewelry demand, which represents about 55% of overall demand, was down 6% versus the two-year quarterly average, down 8% quarter-on-quarter and down 3% year-on-year. Investment gold, such as bars and coins, which represents about 23% of overall demand, was down 20% in Q1/15 versus the two-year quarterly average.

Source: World Gold Council Demand Trends Q1/2015 and Canaccord Genuity estimates

Source: World Gold Council Demand Trends Q1/2015 and Canaccord Genuity estimates

TGR: Are the central banks still buying?

JM: Purchases in the last documented quarter, Q1/15, were about 119 tonnes, so still positive. However, that is down 18% versus the two-year quarterly average. Of note, there was a positive inflow of ~26 tonnes in exchange-traded funds (ETFs) during Q1/15, the first net inflow in a protracted period of time. The two-year quarterly average for ETF investments was a net withdrawal of about 111 tonnes. So much of the negative demand equation was offset by that net inflow. We don't believe that we will see the same positive impact from ETF investments in Q2/15, however.

TGR: Is continued gold production threatened by a gold price under $1,100/oz?

JM: We highlight that the Q1/15 mine supply net of hedging, 734.2 tonnes, according to the World Gold Council, was down 7% versus the two-year quarterly average. The only reason overall demand remained flat—1,089.3 tonnes—versus the two-year quarterly average was a spike in the supply of scrap gold (+17% versus two-year quarterly average, 355.1 tonnes).

"Asanko Gold Inc. is advancing the first phase of the Asanko gold mine in Ghana."

The impact of a lower gold price on mine supply lays the foundation for a healthier gold market in the medium to long term. We highlight that over the next 5–10 years, production curtailments combined with the lack of capital spent on development projects and significant cut backs in exploration expenditures will challenge future mine supply. The paucity of projects may drive future M&A bids for junior companies with quality assets in manageable jurisdictions that are currently well funded to production due in part to the quality of the management team. In our opinion, these are the companies that investors should seek.

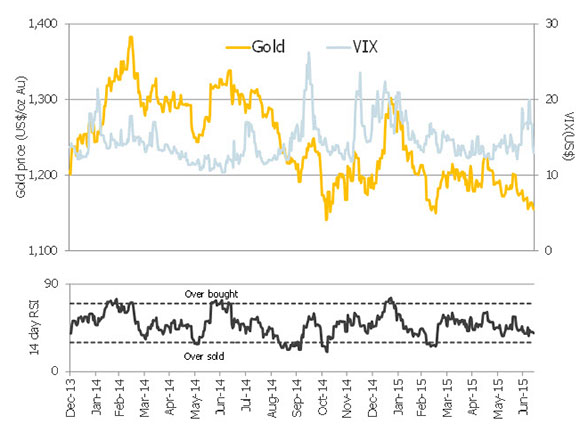

TGR: The gold price has collapsed during a period of burgeoning economic and geopolitical volatility. So is gold no longer a safe haven?

JM: Gold has recently lost some of its attraction as a safe-haven asset. Normally, a spike in market volatility as proxied by the Chicago Board Options Exchange Volatility Index (VIX) results in an uptick in safe-haven assets such as the U.S. dollar and the gold price. These assets are historically negatively correlated except for periods of high market volatility that generate a bid for safe-haven assets. We observed a spike in the Chicago Board Options Exchange Volatility Index (+40%) from Dec. 28, 2014, to Jan. 16, 2015, with a subsequent lift in the U.S. dollar, the gold price and the Market Vectors Junior Gold Miners ETF (GDXJ:NYSE.Arca), which has a large beta to gold.

Source: Bloomberg

Source: Bloomberg

From June 23 to about July 7, 2015, when the Greek crisis was at its peak, the Chicago Board Options Exchange Volatility Index spiked up 60%. But unlike the previous spike, gold was flat to down. Some cite the collapse of the Chinese stock market as a partial reason for the muted response from the gold price. When margins were called, investors had to sell liquid assets and this may have included gold holdings. This selling may have triggered further stop-loss selling in a low liquidity environment (summer market) placing further downside pressure on the gold price. The current sentiment remains pessimistic as investors increased their short positions in gold.

TGR: The price of gold falls in U.S. dollars even as the U.S. dollar rises against other currencies. So does this mean that Canada and other non-American mining jurisdictions, such as Australia, are riding out this storm?

JM: Yes. At the start of the year, one U.S. dollar was worth CA$1.16. It's now worth CA$1.30. So the Canadian dollar is down 12–13% in 2015, which means that the gold price in Canadian dollars is actually up 3–4%. So we favor miners with high-grade Canadian assets.

TGR: Given that Canadian gold producers still make money, and their market caps are discounted by 30%, can we expect a flurry of takeovers?

JM: Yes, but we suspect that this might be put off while investors and potential merger and acquisition (M&A) suitors wait for the Canadian dollar to fall even further. Note federal elections in Canada are planned for Oct. 19, 2015. The current polls suggest that the right-leaning Conservative party and the left-leaning New Democratic Party are neck and neck. The potential for a minority or coalition government with an economy teetering on recession due in part to a weak commodity complex could place further pressure on the Canadian dollar.

TGR: Will much of this M&A activity come from China?

JM: Chinese state-funded organizations are definitely interested in gold-copper assets. An executive director of Zijin Mining Group Co. (601899:SHA), George Fang, has stated that "gold is our game." Zijin Mining Group began 2015 by acquiring a 9.9% stake in Pretium Resources Inc. (PVG:TSX; PVG:NYSE) for CA$80 million (CA$80M) in January. In March 2015, the state-owned company purchased a 9.9% stake in Ivanhoe Mines Ltd. (IVN:TSX│Not rated) for CA$105M (US$83M). Subsequently, in May 2015, Zijin Mining agreed to co-develop the Kamoa copper project by acquiring a 49.5% stake in the project for US$412M.

"Pretium Resources Inc. is on the Canaccord Genuity Focus List as it represents a high-grade gold development play in a stable jurisdiction."

Barrick Gold Corp. (ABX:TSX) signed a strategic relationship in May 2015 with Zijin Mining; the first step involved having the Chinese state-owned mining company purchase 50% of the Porgera gold mine joint venture in Papua New Guinea for US$298M. In June 2015, Zijin Mining also launched an AU$47M bid to acquire Phoenix Gold Ltd. (PXG:ASX) for its Australia-based gold assets.

So overall, we estimate that Zijin Mining has made a total of approximately US$900M in investments in gold and copper assets in Canada, Africa and Australia. Going forward, we anticipate further M&A and investment activity by Chinese state-owned mining companies given the current weak market conditions.

TGR: Are the Chinese investing in Canadian gold companies with a view to growing China's gold reserve?

JM: China is the world's leading gold producer and its largest gold mine, Zijinshan gold-copper mine in Fujian province, which produced 331,800 oz (331.8 Koz) in 2014 (Source: SNL), is operated by Zijin Mining. To augment domestic production, Chinese firms are acquiring assets in other countries such as Canada, Africa and Australia, among other jurisdictions. Given current valuations, it may be cheaper for them to purchase assets or fund management teams with an underlying offtake agreement rather than buy gold.

TGR: Let's talk about specific companies. Canaccord Genuity recently raised its 52-week target price on which near-term gold producer?

JM: Torex Gold Resources Inc. (TXG:TSX). We rate it a Speculative Buy and on July 22 raised its target price from CA$1.40 to CA$1.60. This followed the July 21 release of the company's preliminary economic assessment (PEA) on its Media Luna gold-copper project in Mexico. The Media Luna project falls within the 29,000-hectare (29,000 ha) Morelos gold property, which also includes the El Limón-Guajes (ELG) project that is currently under construction. The majority (~95%) of our Torex valuation is based on its high-grade open-pit ELG gold project, which is now 80% built, with first gold pour scheduled for Q4/15 and commercial production by Q3/16, according to our estimates. Half of our target increase was related to the improved grade and throughput profile outlined in the updated ELG mine plan. The other portion of the target price increase was related to the impact of the Media Luna PEA.

TGR: Are investors confused by Morelos and its different elements?

JM: Media Luna presents further upside potential and reflects management's attempt to quantify its 29,000 ha land package while attempting to leverage the infrastructure currently being put in place. This includes adding a flotation circuit at the ELG plant facility and using mined-out open pits to dispose of tailings. Logistically, Media Luna's integration into El Limón-Guajes presents a number of engineering challenges as Media Luna is on the other side (south) of the Rio Balsas. The upfront capital expenditure estimate of US$480M in the July 2015 PEA incorporates both aerial and underground rope conveyors to transport the ore to the ELG plant and underground tunnel access to the deposit.

Source: Torex Gold

Source: Torex Gold

Torex Gold's share price has been negatively impacted by the lower gold price and the security risks in the Mexican state of Guerrero, where Morelos is located. However, Torex Gold has still outperformed the Market Vectors Junior Gold Miners ETF benchmark in 2015 year-to-date (down 9.3% versus down 20.1%). The good news for Torex Gold is that there have been no significant security incidents over the past few months.

TGR: Which gold companies operating in Canada have you rated Speculative Buys?

JM: Pretium, Claude Resources Inc. (CRJ:TSX) and Rubicon Minerals Corp. (RBY:NYSE.MKT; RMX:TSX).

TGR: What do you like about Claude?

JM: Over the past 12 months, Claude Resources has easily outperformed the Market Vectors Junior Gold Miners ETF benchmark (up 134% versus down 55%). The keys to its success are underpinned by positive cash flow from operations from a high-grade resource, Santoy Gap, within a stable geopolitical jurisdiction, Saskatchewan, operated by a management team with the technical expertise to take advantage of the options that underground mining presents. Consistently high metallurgical recoveries of 95–96% are also a positive. Its cost exposure to the Canadian dollar is about 95%, so any further weakness is considered favorable.

Source: Claude Resources and Canaccord Genuity estimates

Source: Claude Resources and Canaccord Genuity estimates

Claude's ability to convert its non-reserve (NRM) resource base, specifically at Santoy Gap, is a critical risk component of its future success, as currently its 2P reserve base accounts for approximately four years of production. We have modeled a Life-of-Mine plan based on a mineable resource of 824 Koz grading ~6.8 grams/tonne gold (~6.8 g/t Au) (70% of global resource of 1,167 Koz grading ~7.6 g/t Au) after adjusting for conversion risk, mining dilution and recovery of its NRM resource base. Claude Resources is planning on a significant drill program—60,000 to 65,000 meters (65,000m)—at Seabee and Santoy Gap to upgrade the resource base. The Seabee property in north-central Saskatchewan comprises a significant land holding of 19,950 ha as of late June 2015. In our opinion, given its balance sheet strength, Claude can fund a sustainable growth profile organically.

TGR: What do you like about Rubicon Minerals?

JM: We lowered our target price—down CA$0.30 to CA$1.50—in early July 2015 due to a negative revision in our commodity price forecasts and the impacts of a slower ramp up to commercial production (Q1/16E) with lower head grades. However, as our target price still represents a +35% implied return to current levels, we maintained our Speculative Buy rating.

Rubicon Minerals represents a dual-listed, well-funded, high-grade underground gold development play with a significant land package—100 square miles—in the highly sought Red Lake District of northwest Ontario in Canada. Adding near-surface ounces proximal to the plant infrastructure, currently in construction, would be a positive, in our opinion, that could defer some of the major capital expenditures required for vertical development at the F2 Zone. Rubicon's management has prior relevant underground mining expertise in the Red Lake area with Goldcorp Inc. (G:TSX; GG:NYSE). The company announced its first pour of 741 oz in late June 2015.

One of the risks is that the company has yet to provide guidance to commercial production. We note that some companies developing underground projects have declared too soon and then run into issues, so we believe the company is being cautious to ensure an achievable target.

TGR: How close to being permitted is Pretium's Brucejack project?

JM: Pretium got its British Columbia provincial permit in late March 2015, which at the time was ahead of our forecast. The company recently acquired the Federal approval from Minister of the Environment after a review by the Canadian Environmental Assessment Agency (CEA). With receipt of the federal permit, the company will issue a notice of construction and we expect the beginning of earthworks by the latter part of August 2015. Pretium ended Q1/15 with a working capital position of CA$103M. After the release of the financials, we believe the company will present a project update with guidance on financing by late August to September 2015.

In the interim the company has not been sitting on its hands.

The majority of the gold development companies we cover are working to quantify the upside of their land packages in parallel with advancing their primary asset. This is important if M&A activity picks up, and Pretium is no different. The prospectivity of its approximately 104,111 ha land package for porphyry related to epithermal precious and base metals is well established. We continue to be impressed by the methodical detail and thought reflected by the company's exploration efforts on its extensive land package. The company is planning up to 15,000m of drilling at the Flow Dome and Kitchenview zones, high priority targets delineated by their regional exploration program.

Source: Pretium Resources

Source: Pretium Resources

TGR: Pretium's recent infill drill results are about the same quality it was getting a couple of years ago, right?

JM: Yes. The primary goal of Pretium's 2015 underground infill drill program (40,000m, 3 underground drill bays, 32 drill fans, 10m centers) is grade control within stopes defined by the 2014 feasibility study for the first few years of planned production at the Valley of Kings (VOK) deposit.

Recent results of 9,003m drilling included 164.54 g/t over 13.75m, 259.48 g/t over 10m and 83.89 g/t over 15m, which serve to confirm the high-grade mineralization outlined in the 2014 feasibility study. The Valley of Kings is a high-grade deposit with a volatile grade profile, which makes it controversial. We have discounted the head grade (12.5 g/t Au vs. 14.1 g/t Au) and throughput (2000 tonnes per day [2.0 Kt/day] vs. 2.7 Kt/day) to account for grade volatility.

We recently reduced our Pretium target price from $8.50 to $8.00, due to a downward revision in our long-term commodity price outlook, but that still represents a significant premium (25%) over the current price. Pretium is on the Canaccord Genuity Focus List as it represents a high-grade gold development play in a stable jurisdiction with the downside risk mitigated somewhat by its strategic investor (Jan. 16, 2015, CA$6.30, CA$80M), the Chinese state-owned mining company Zijin Mining, which has been highly active in mining acquisitions/investments in 2015.

TGR: Let's talk about companies you like in West Africa.

JM: I'll mention two. The first is Asanko Gold Inc. (AKG:NYSE.MKT; AKG:TSX), which is advancing the first phase (P1 Obotan) of the Asanko gold mine in Ghana through commissioning (Q1/16E) to commercial production (Q2/16E). We recently upgraded Asanko from Hold to Speculative Buy as our target price (CA$2.60) implies a +30% return to current levels. Year to date in 2015, Asanko has outperformed the Market Vectors Junior Gold Miners ETF benchmark (up 11.6% vs down 19.1%).

TGR: How do you rate the Asanko phase 1 ramp up?

JM: I think excellent as P1 Obotan construction is 60% complete with 2,400 personnel on site and on schedule for first pour by Q1/16 leading to cash flow positive commercial production (Q2/16), in line with our forecasts. All critical path items are in hand and on schedule, according to the company. Mining is advancing faster than planned (100 Kt/day, +10%) as the contractor has mined over 7.9 million tonnes (7.9 Mt) of the required 21.7 Mt of pre-stripping for Nkran. Importantly, dewatering has pumped out 56% or 3.36 million cubic meters (3.36 Mm3) of the 6 Mm3 required at the Nkran pit, which hosts the largest mineable resource base (>85%) at P1 Obotan. The water level has fallen 24m since dewatering began in December 2014. Another critical item is the partial relocation of the Nkran village (88 buildings), which is on track for the end of Q3/15.

Source: Asanko Gold

Source: Asanko Gold

As power availability and reliability is a critical issue in Ghana, Asanko's management has signed a deal with an independent power producer, Genser Energy Ghana Ltd., to secure power to the site. We estimate that ~45% of Asanko's processing costs are related to power. The company is also progressing on its 30 kilometer (30km) 161 kV power line (Q3/15E completion) to connect to the power grid. Under the power purchase agreement (PPA), Genser Energy as operators will have the right to utilize the power line to sell excess power onto the grid or to supply through the grid. The PPA also provides Asanko some security and flexibility with respect to power needs during ramp-up of the 3 Mt/year processing facility at Nkran.

TGR: And the other West African company you like is?

JM: Roxgold Inc. (ROG:TSX.V), which is also rated a Speculative Buy, is advancing its high-grade, underground Yaramoko gold project. Its shares had previously suffered due to the political uncertainty in Burkina Faso and more recently because of the gold price drop. But despite these headwinds, Roxgold has outperformed the Market Vectors Junior Gold Miners ETF in 2015 year-to-date (up 12.7% versus down 19.1%).

Its outperformance can be linked to the high internal rate of return generated by the project due to the high-grade nature (>11 g/t Au, our estimate) of the deposit combined with the low upfront capital forecast (US$120M, our estimate).

Source: Roxgold Inc.

Source: Roxgold Inc.

Also, the positive performance is attributable to management's delivery of a number of positive milestones including the signing of its mining agreement with the interim government of Burkina Faso based on the 2003 mining convention, which should keep the corporate tax rate at 17.5% versus the new rate of 27.5%. However the Yaramoko gold project will probably still be subject to a new 1% net smelter royalty.

Management also successfully closed its US$75M debt facility while receiving a positive endorsement from the International Finance Corp. via a private placement of $18.4M in late June 2015.

The company has begun construction activities at Yaramoko's 55 Zone with bulk earthworks well advanced. The company excavated the boxcut for the underground portal. With the plant site earthworks complete, the engineering, procurement and construction contractors (DRA/Group 5 JV) and mining contractors (AUMS) have mobilized to site. We forecast commissioning in Q2/16, in line with company guidance, leading to commercial production by early H2/16E for the 55 Zone of the Yaramoko gold project.

Another reason we like Roxgold is its extensive and prospective land package. We have modeled a higher mineable resource estimate (+20%, 920 Koz) than the April 2014 feasibility study (759 Koz) to quantify the potential upside. The company has designed a scalable plant that could be upsized by 50% at a reasonable cost, US$5M, if more feed is found.

TGR: Do you like any Canadian gold companies operating in Europe?

JM: Dalradian Resources Inc. (DNA:TSX) is advancing the Curraghinalt project in Northern Ireland. Like Pretium, Dalradian is on our Canaccord Genuity Focus List. We rate Dalradian as a Speculative Buy with a $1.30 target price. Few companies were able to finance in 2014, and many fewer managed to finance twice like Dalradian. Both of the company's equity financing transactions were oversubscribed and the second one was upsized to accommodate demand. Demand was supported by a strategic investor, Ross Beaty, who provided a positive endorsement for both the management team and the asset. Its board has been strengthened with some natives of Northern Ireland.

Curraghinalt represents another high-grade, underground gold project, with a potential head grade of 8.3 g/t, according to our estimates. It is in a stable jurisdiction, Northern Ireland, which is not as well known a mining jurisdiction as the Republic of Ireland, but has a good workforce and is mining friendly. Results gathered during a March/April 2015 survey of the local community indicated that the majority—70%—have a positive inclination to the development of the Curraghinalt project.

In June 2015, Galantas Gold Corp. (GAL:TSX.V) received planning consent for its Omagh underground gold project, 20–25km southwest of Curraghinalt. We consider this a very encouraging precedent.

We note that the Omagh project produced a gold and silver-rich sulphide concentrate that was shipped and sold to a smelter from the open-pit and the processing method will not change (i.e., no cyanide) going forward with a potential operation underground mine. We continue to model a concentrate-only circuit for Curraghinalt to avoid the use of cyanide at site and lessen its permitting risk. Dalradian is currently studying processing alternatives including a flotation circuit, and we suspect that priority will be given to those that are acceptable to the local community with lower technical risk at a reasonable cost.

TGR: How is Curraghinalt being derisked?

JM: Dalradian is currently executing its underground exploration program at the Curraghinalt project, which comprises 20,000m of drilling from surface (5,000m completed) and underground (15,000m) with an additional 1,000m of geotechnical drilling. The drill program covers 45% of the 1.7km strike length of the last reported Curraghinalt resource to a depth of ~400m from surface. The focus is to upgrade resource ounces from Inferred to Indicated leading to a resource update (Q3–Q4/15E) to support a prefeasibility study (PFS) by late 2015 to early 2016. The company's COO, Eric Tremblay, will lead the PFS and underground program as he provides extensive (25 years) and relevant (mostly underground) development and operations experience, most recently as general manager of the Canadian Malartic gold mine.

The company reported results from 5,766m (25 holes) of predominantly surface drilling (23) and two holes from underground predominantly targeting 3 veins (T-17, No. 1, V-75, Bend and Crow veins). Highlights included 4.4m grading 54.84 g/t Au, 5.79m grading 7.12 g/t Au and 4.74m grading 15.26 g/t Au.

The CA$13M underground program will also include 1,100m of total development, including 440m of access drifting to crosscut four southern veins (Crow, Bend, V75 and 106-16) and an additional 430m related to on-vein development (T17 and No. 1). Hydrogeology and geotechnical studies combined with metallurgical test work will be ongoing.

TGR: We've had innumerable false dawns since the bear market started in April 2011. You told us you don't believe the gold price is going significantly higher in the near future. So what sort of projects should investors in gold equities be in?

JM: With respect to gold investors, it depends on whether you're a generalist or a goldbug. The latter doesn't need to be persuaded that gold is going much higher, and will tend to bet on highly levered plays. We do not recommend purchasing illiquid companies that are seeking to fund the advancement of a marginal deposit. The fact that our gold price forecast is basically the actual gold price futures curve at the time reflects our acknowledgement of the difficulty in forecasting the gold price with any accuracy. We prefer to recommend companies with quality projects that generate a double-digit internal rate of return at current price levels and reside in stable or manageable geopolitical risk jurisdictions within significant and prospective land packages operated by management teams with relevant experience—technical, execution and financial.

Hence, my Focus List picks—Dalradian and Pretium—represent high-grade gold projects in Canada and Northern Ireland—stable jurisdictions with significant land packages and management teams that continue to advance their respective projects while attracting strategic investors.

Finally, as a hedge to a downward trajectory in the U.S. dollar-denominated gold price, we would also focus on assets in jurisdictions with resource-based economies such as Canada, Australia and Brazil. All these currencies have fallen against the U.S. dollar; hence the local gold price is higher than the U.S. dollar quote. Personally, I prefer Canada.

In the current gold market environment, high-grade underground in Canada represents the best of all possible worlds for me. Investing in a small but profitable producer operating a high-grade underground gold mine on a large land package in Saskatchewan such as Claude Resources would also be a decent bet in the current market environment.

TGR: Joe, thank you for your time and your insights.

Joe Mazumdar is a senior mining analyst focused on the junior gold market at Canaccord Genuity. Prior to that he was at Haywood Securities, where he also was a senior mining analyst. His experience includes director of strategic planning, corporate development at Newmont and senior market analyst/trader at Phelps Dodge. Mazumdar also worked in technical roles for IAMGOLD in Ecuador, North Minerals in Argentina/Chile and Peru, RTZ Mining and Exploration in Argentina and MIM Exploration and Mining in Queensland, Australia, among others. Mazumdar has a Bachelor of Science in geology from the University of Alberta, a Master of Science in geology and mining from James Cook University and a Master of Science in mineral economics from the Colorado School of Mines.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Pretium Resources Inc. and Asanko Gold Inc. Goldcorp Inc. is not affiliated with Streetwise Reports. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Joe Mazumdar: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. Canaccord Genuity disclosures available here. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.