On Tuesday of last week, America delivered a resounding verdict on the Biden-Harris presidency, returning former President Donald Trump to office with a landslide victory with 301 electoral college votes versus 226 for the Harris-Walz ticket. During the overnight electronic trading session, stock index futures and the U.S. dollar moved in direct correlation to the Trump victory march, and by the opening of the NYSE the following morning, the Dow Jones Industrial Average was up over 1,200 points.

It is not my task to dissect the election results but rather to rejoice in the manner in which the outcome was accepted, with nothing in the form of social or civil disturbances to mar the process. Victory laps by the winning candidates were tasteful and muted, while concession speeches were absent any of the finger-pointing that accompanied those in 2020. In the end, it was the unanimity of the American voters that solidified not only the outcome but also the reaction (or lack thereof) to the crushing Trump victory. That Trump took 39 of 50 states with Republican victories in the Senate and a substantial lead in the House (215-208) remains a stark testimonial to the widespread rejection of the policies and personalities of the Harris-Walz campaign. However, from a market perspective, with the ideal outcome being gridlock where the losing party controls either the House or Senate, three more Republican votes in the House will constitute a complete sweep and enable the realization of more than a few market-hostile campaign promises to be voted into law.

Lower taxes and/or tariffs on imported goods would not be a positive development for growth as less government revenue would seriously impair the fiscal imbalances associated with a $36 trillion debt load while tariffs would render imported good far more costly and bode poorly for the inflation fight.

Nonetheless, the election result juiced the three major averages (DJIA, S&P, and NASDAQ) to record highs and even kick-started the small-cap Russell 2000 to a record high while the hedge fund community, seriously underweight equities going into the election, scrambled to top up their allocations for the remainder of the week.

Fortunately, for the first time in decades, I went into U.S. election week completely unhedged with zero positioning in either put options or volatility, which for me was a departure from past election events. However, despite owning the Invesco QQQ ETF (QQQ:NASDAQ) from $490 as well as a few call options for December delivery, the bulk of my portfolio was in the metals, which suffered a week of well-deserved profit-taking after several weeks of uninterrupted uptrend.

A great many hedges were lifted after Tuesday, and gold was certainly one of them, losing 3.8% from the October 1 peak above $2,800. Silver is now down 10.3% from the October 23 peak above $35/ounce, and copper is down 10.1% from its $4.79/lb. peak at the close of September.

Notwithstanding the huge shift in post-election sentiment in the metals, they are really only just checking back to where they were a month ago with overbought conditions now moderated and trendlines very much intact.

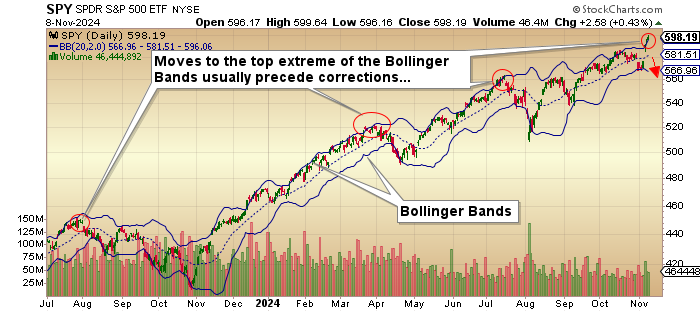

The SPDR S&P 500 ETF (SPY:NYSE) has moved to within a point of "overbought" territory, but the interesting feature of its post-election spike is how it has now exceeded the upper realm of the Bollinger Bands, which has historically led to corrections in the past fifteen months. While that is certainly cause for cooler heads to prevail, the only thing keeping me from getting seriously short the S&P is the trillion dollars of corporate buybacks idling out there and ready for launch.

Mind you, how much of that buying was expended after Tuesday has yet to be revealed, but with the SPY up 27.04% YTD, one has to wonder how much more upside there is to a market not only priced to perfection but now illuminated by the pro-growth Trump presidency?

I wrote of the possibility of a year-end "melt-up" due to the buybacks once the election result was rendered, but after watching stocks go "no offer" last week, I am leaning toward the view that last week may have actually exhausted the latent bullish impact of both corporate buybacks and a Republican sweep. It will all come down to positioning and how the large mega-funds are allocated going into year-end. I suspect that they are now quite bullishly postured, and if that is true, the gunpowder in the S&P cannon will be somewhat spent compared to where it was a week ago.

I have tightened up the stops on the QQQ to $510.00, and I shall continue to raise the stop until a reversal takes me out. I cannot, in all honesty, tell the world that I am going to short this market, but I will confess to wanting to. There are a great many risks out there, and whenever I watch the CNBC anchors all chortling and giggling over the record highs in the averages, I am reminded of prior periods where their jocularity was symptomatic of a secular market top.

We shall see. . .

GDX

The VanEck Gold Miners ETF (GDX:NYSEARCA:) had a difficult week, and unlike the physical metals where the pullbacks have yet to alter their bullish chart patterns, the GDX actually began to correct during the third week of October, thanks in no small degree to the disastrous earnings report by Newmont Corp. (NEM:NYSE) that cratered the stock and thanks to its massive weighting in the HUI, the XAU, and in the GDX, took the entire sector down in an across-the-board liquidation binge.

The miners had been correcting in the two weeks prior to last Tuesday, but as the dollar soared in response to the Republican victory taking the metals sector down through the floorboards, it intensified the drop in the big gold miners, causing the GDX to shatter its wonderful uptrend line that had been rock solid since the late-February lows. We absolutely must see that line reclaimed next week, or else the May-June lows of around $33 will be in the cards.

Also, making a complete idiot out of me has been silver as I urged the world two weeks ago to "Hail the Silver Bull" and cited about 500 reasons why everyone should not jump but pole vault enthusiastically onto the Sprott-ian bandwagon. Silver prices took one look at my bullish missive and summarily dismissed any notion of $50.00 silver such that by the following Tuesday night, a near-term top had formed thanks largely to the protruding middle fingers of the bullion bank traders that rejoined their commonplace habit of selling technical break-outs and buying technical break-downs.

It was Albert Einstein who was quoted as defining the term "insanity" as "behaviors repeatedly exhibited over and over only to result in the same negative outcome," and that is precisely how I would characterize my trading prowess in the silver market these days.

Now that I have admitted my human mortality (and intellectual frailty), I am inclined to ignore the current dreadful sentiment in the shiny metal because if the social media website otherwise known as "X" and formerly known as "Twitter" is any indication; then we should all be buyers because the week of October 21-28 when the polls were indicating (incorrectly) a Harris-Walz victory and silver was gapping north of $35/ounce (basis December), the walls of that social media website were reverberating with the sounds of podcasters and newsletter gurus and mouth-breathing cheerleaders all clamoring to hold the mantle and kiss the ring of the loudest silver bull out there.

Without mentioning names, they were to a man and woman all desperately running victory laps, assigning rapidly recalibrating decimal points to the silver price and, of course, while repeating over and over the memorized mantra as to why silver was going to enrich the masses. After Tuesday of last week, one could hear a pin drop in the halls of social media chatrooms with the mouth-breathers conspicuously absent and embarrassingly silent.

It never fails to amaze me how the price action determines the fundamental narrative, as in the case of a Republican landslide that most certainly mobilized a heretofore unknown and gargantuan supply of unallocated silver that was most surely going to be unleashed upon an already-oversupplied silver market, taking prices back to the post-pandemic lows below $10/ounce. Contrast that newly-found opinion with the narrative of two weeks ago, where the kiddies were hawking their grannies' antiques to buy silver.

Due to these extremes, I am taking the other side of the trade that engulfed the silver market last week and am going to add to my holdings carefully and patiently. With gold residing comfortably above its well-established trendline, there is going to be a multi-month period where silver outperforms gold, and whether silver needs to move even lower in order to set up an oversold condition, I will soon know by the middle of next week. Despite being monkey-hammered by the false break-out of two weeks ago, I remain of the opinion that a $3,000 gold price and gold-to-silver ratio of 65 is a strong possibility before this metal's bull expires.

That implies a realistic price objective, not "to da moon," not "$200 silver" (followed by 27 exclamation marks), and not caused by shortages but rather based upon its time-tested relationship to gold. Period.

The Junior Explorers and Developers

Up until at least last Tuesday, I sensed a dramatic clearing of the log jam in the junior resource industry's funding problems. While the corrections in the metals exacerbated by the Republican landslide may have postponed the party for a while, I made note of a distinct shift in sentiment for the juniors in October.

Assuming no further steep declines in the gold, silver, or copper markets, I see the funding market heating up as we approach the New Year and, with it, the valuations for the higher-quality junior issuers that populate the TSX Venture Exchange.

The TSX Venture Exchange was humming along quite merrily until around the third week of October when the metals topped out, and since then has been tracking price movements in gold and silver to a tee. What I am noticing is that solid stories are starting to attract interest, and while we are nowhere close to the pre-GFC period or the 1990s boom era, a recovery in retail and institutional interest will be a welcomed event for a group of risk-takers who are largely responsible for many if not all of the world's major resource discoveries of the past 50 years.

The juniors find it, and the seniors develop it, but not before the seniors write big fat cheques to acquire it.

| Want to be the first to know about interesting Critical Metals, Silver, Base Metals and Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Michael Ballanger: I, or members of my immediate household or family, own securities of: All. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

new.jpg")