Chalice Mining Ltd. (CHN:ASX; CGMLF:OTCQB) is a super stock for the next decade.

I still think an AU$20 target is on track for a few years out.

The company has a market cap of US$450 million on 389 million shares at AU$1.15 and AU$111 million in cash.

Palladium price is also finally about to surge.

One of the Great PGM Discoveries

The Julimar PGE Project, delineated at Gonneville, is one of the great PGM discoveries of the century. Its high Palladium content, together with copper, nickel, and other minor contributors, makes it a very attractive low-cost mining and high-margin operation once it is up and running.

The substantial decline in Palladium prices from US$3400 in early 2022 to as low as US$800 in the past month would have made most Chalice shareholders a bit concerned about the future. All the negativism that goes with low prices was widely spread, but just watch it evaporate as palladium heads higher again.

We all know that what goes up must come down, and what goes down will eventually go up.

The particular case of palladium has been this drawn out 40 month C wave that has created the pessimism that a wave 2 always exhibits.

And, of course, when wave 2 finishes, wave 3 begins, which it is doing now. That means new highs are coming. This extended basing has gone on for over eight months and has been in the face of improving demand and quite limited supply, particularly from recycling.

This has left deficits, and the deficits of the past four years are likely to continue for the next four years, at least before Gonneville comes on stream.

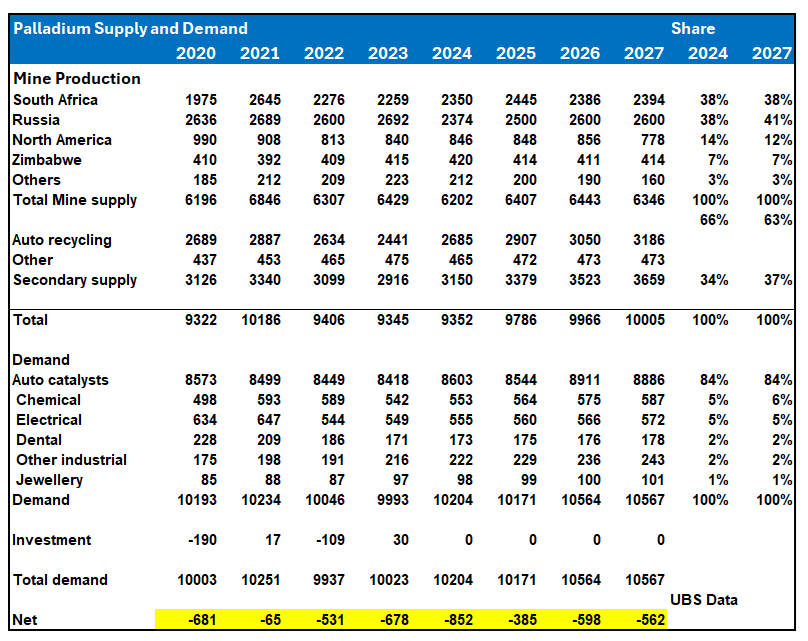

Palladium Supply and Demand

This is a table published in April 2024 showing the run of deficits from 2020 are likely to extend out to at least 2027.

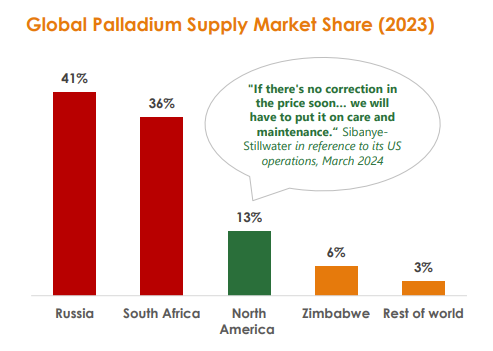

Primary mine supply accounts for about 66% of all refined palladium, with Russia and South Africa sharing equal shares.

Auto recycling is expected to increase from 85% of scrap to almost 90% before 2030 and makeup ~37% of all refined palladium supply.

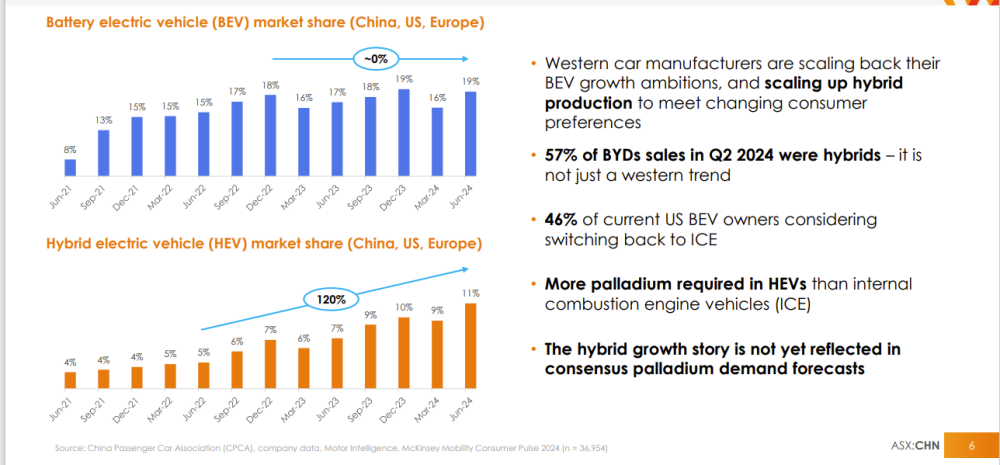

Palladium demand growth is all about auto catalysts for ICE vehicles.

The decline in ICE demand has been less than expected, with Hybrid EVs now more popular and actually requiring more palladium than ICE vehicles. Fewer scrapped ICE vehicles have reduced recycled palladium, so the net result is market deficits.

Where will the palladium inventory come from to meet these deficits?

Battery EV growth has stalled, but Hybrid EVs are increasing market share — good for palladium.

These deficits mean higher prices and, expectedly, new highs in the not-too-distant future.

Note: the imbalance of the supply from Russia and South Africa.

Palladium Prices

Commitment of Traders has Commercials as long and Speculators as short.

That is always a good sign at a market low.

Short term — now breaking out.

The medium-term has the completion of 5 waves down in a c wave.

Completion of wave 2 on rising volume shows strong sellers and strong buyers.

Should the buying overwhelm the selling, the sellers would be forced to buy back short positions in a sharp price squeeze.

That is probably happening now.

The long term shows palladium supporting its 20-year uptrend.

The longer-term shows horizontal support around US$800-900/oz.

MPS has defined a near-term Target #1 at US$2,000, which should be achieved within the next 18 months.

Target #2 at US$2,800 could be reached within three to four years, which could be the first year of Gonneville's operation.

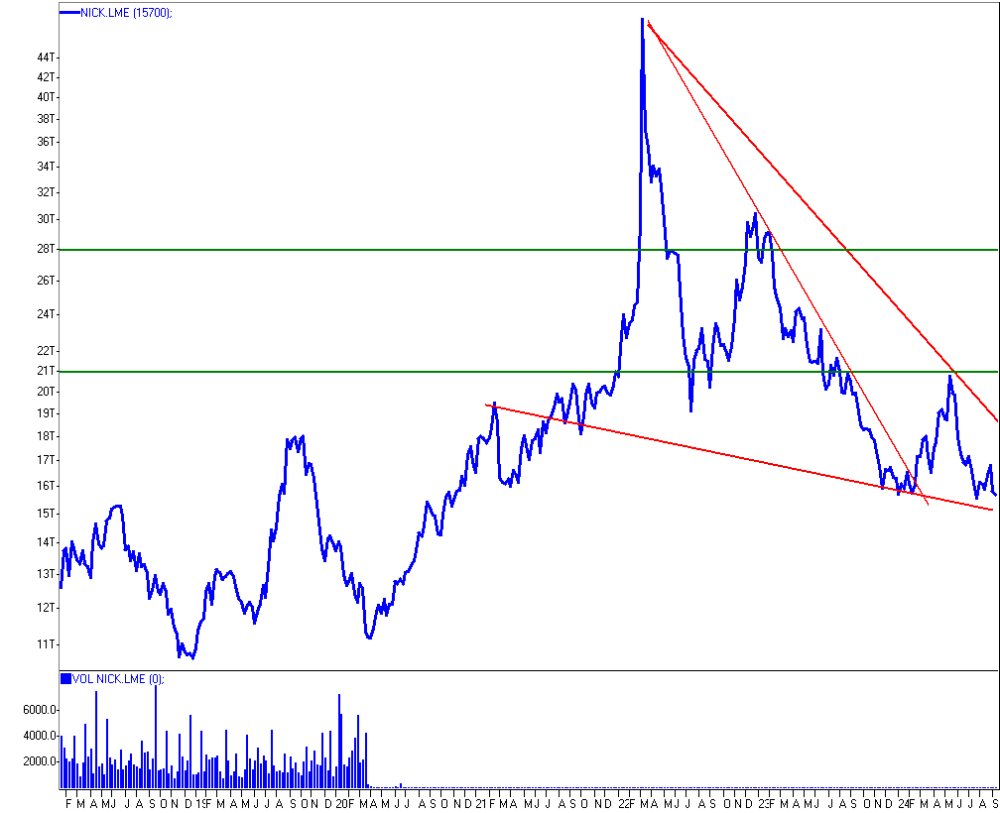

Nickel has displayed a break from a downward-sloping wedge similar to Palladium's and followed it with a very strong rally.

Nickel is testing recent lows, but MPS Target #1 is US$21,000, and Target #2 is US$27,000 within four years.

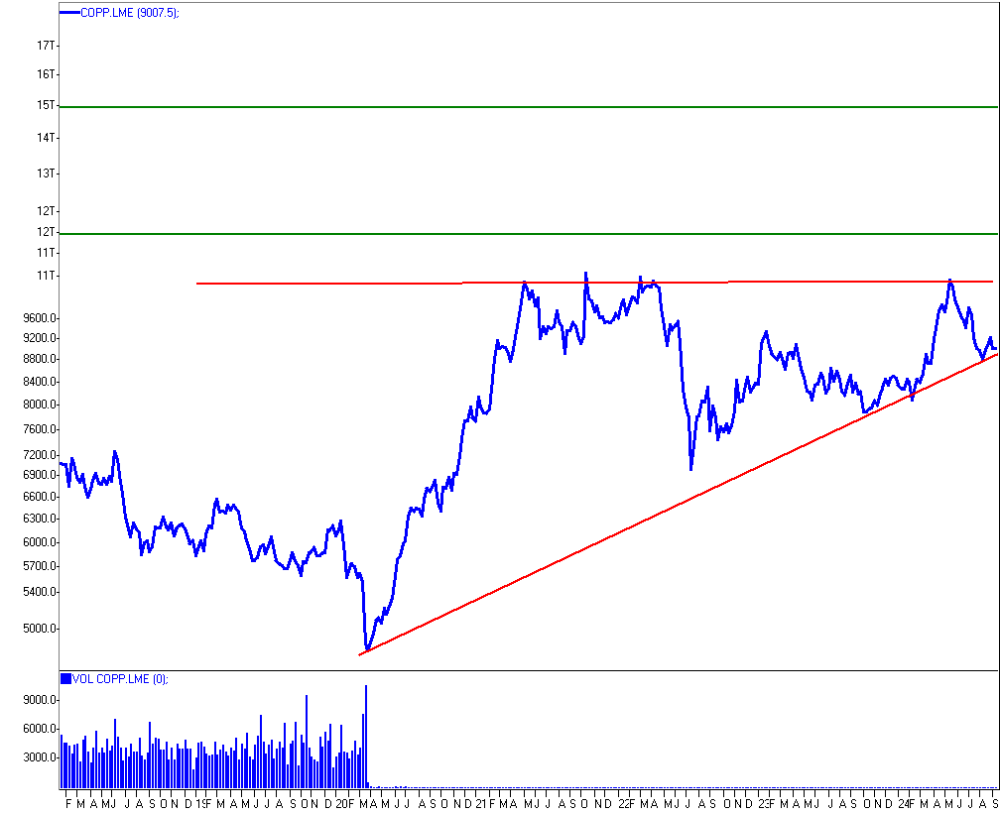

Copper has been promising the world for quite some time, but it is heading higher.

A break above US$10,000 will lead to a very strong rally, so MPS Target #2 at US$12,000 should be soon achieved, and MPS Target #2 of US$15,000 not much later.

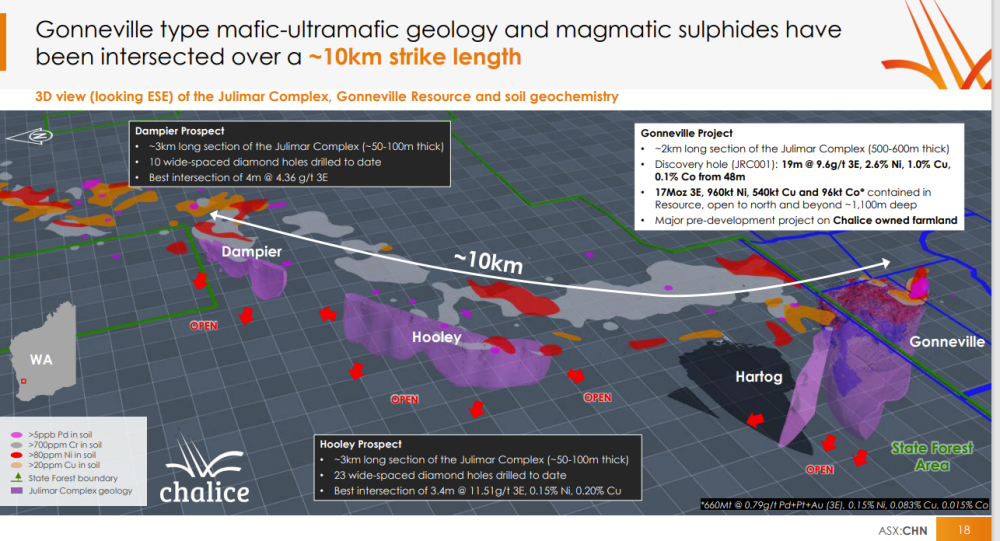

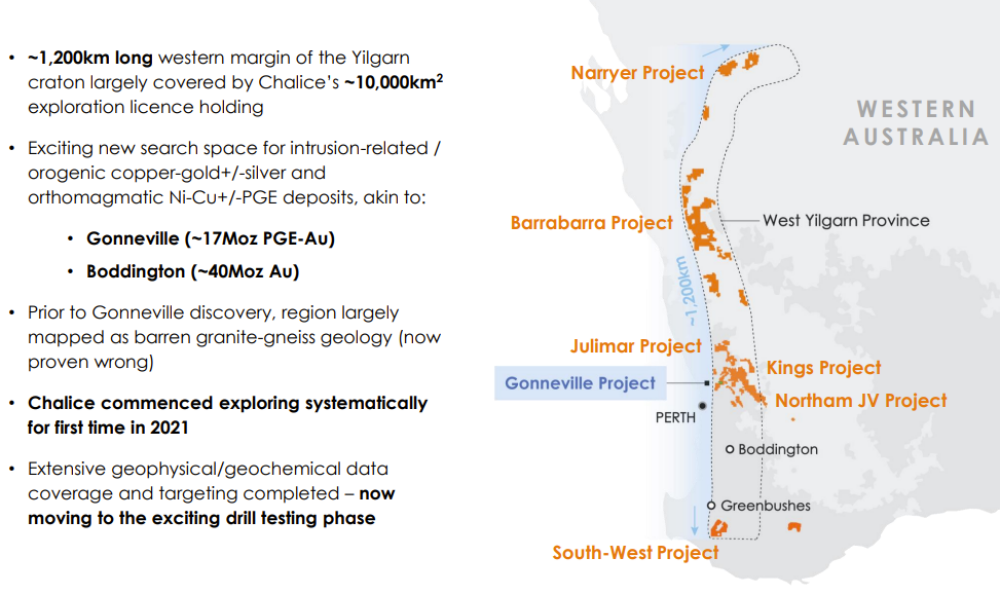

Julimar Complex

This extraordinary deposit of mineralization extends over 10 km.

Gonneville is only the start.

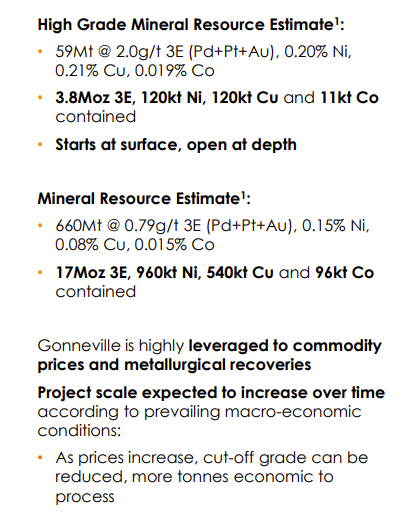

Gonneville Resources

It has 17moz 3E so far in resources and is certainly likely to be much larger over time.

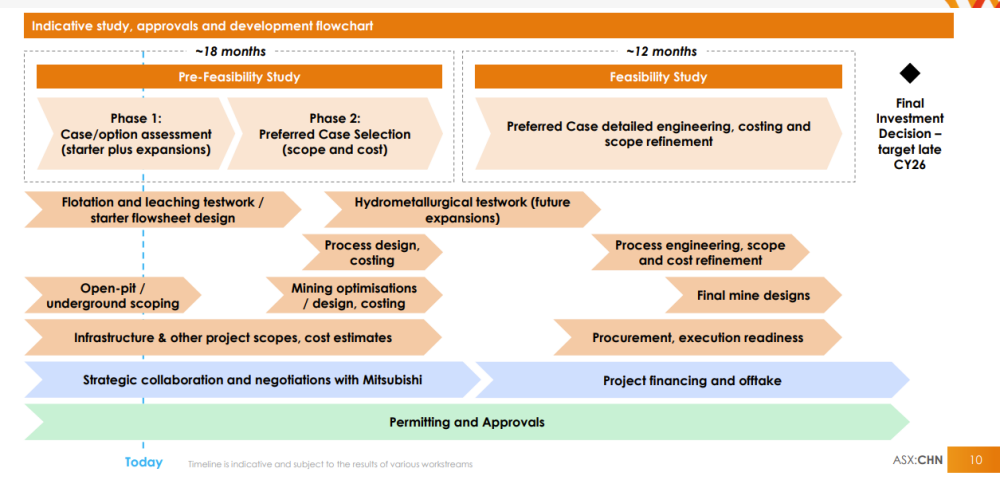

Gonneville Project Development

Latest program:

- PFS mid-late 2025.

- DFS late 2026

- FID late 2026

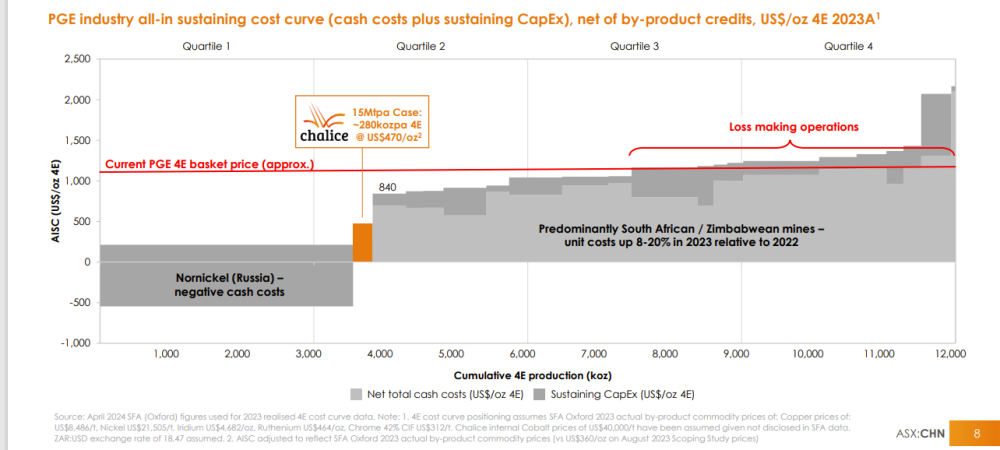

Gonneville will be a very low-cost mining operation, the lowest-cost producer in the Western world, and will sit at the low end of the Second Quadrant of costs.

The Gonneville Project will be developed on the basis of competitive low operating costs but will anticipate long-term higher prices in the coming years.

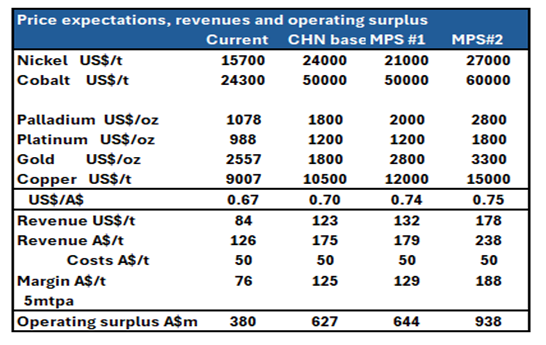

MPS targets over the next few years are as follows:

Current Target #1 Target #2

2 years 4 years

Palladium US$/oz 1,078 2,000 2,800

Copper US$/t 9,007 12,000 15,000

Gold US$/oz 2557 2,800 3,300

Nickel US$/t 15,700 21,000 27,000

Cobalt US$/t 24,300 50,000 50,000

Platinum US$/oz 988 1,200 1,800

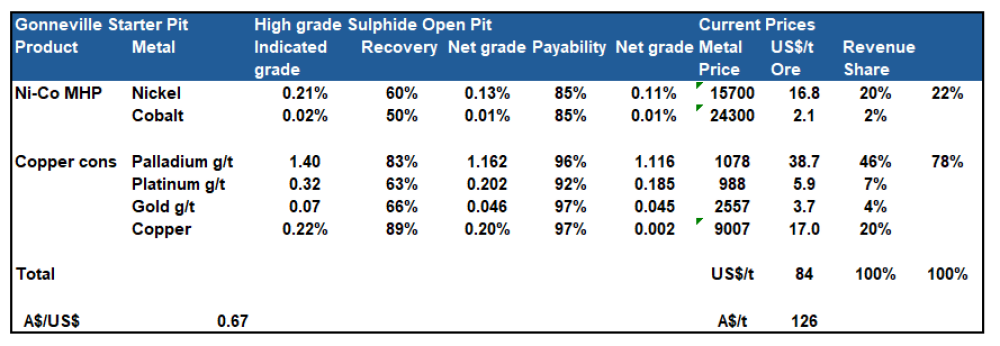

Net Revenue at current prices for the high-grade starter pit with two concentrates produced would show shares of net revenue

- Palladium 46%

- Copper 20%

- Nickel Cobalt 22%

Note that CHN has been making good progress in improving recoveries, so these numbers could be low.

This would give AU$126/t operating margin at current prices.

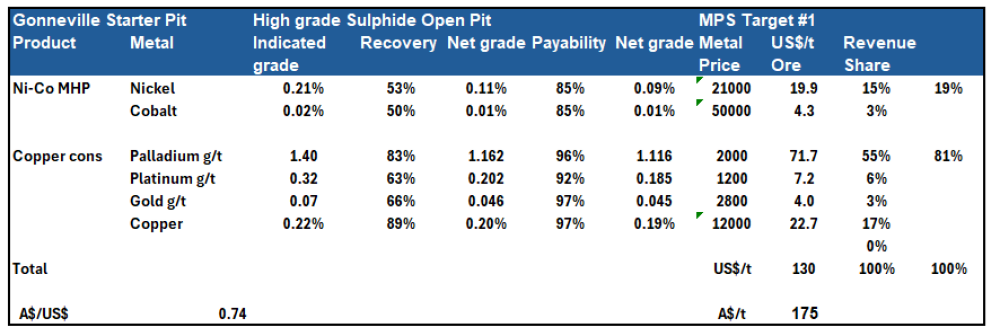

At MPS Target #1, the net revenue would show shares of net revenue

- Palladium 55%

- Copper 17%

- Nickel Cobalt 19%

This would give AU$175/t operating margin at Target #1 prices.

Net Revenues From Concentrates

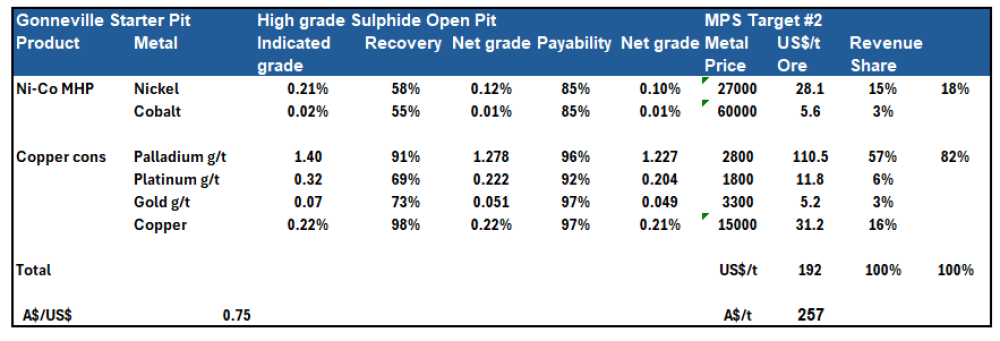

At MPS Target #2, the net revenue would show shares of net revenue

- Palladium 57%

- Copper 16%

- Nickel Cobalt 18%

This would give AU$257/t operating margin at Target #2 prices.

Net Revenues From Concentrates

Turning these net revenue per tonne figures into a 5mtpa starter operation, CHN could be generating significant operating surplusses.

- At current prices AU$380m

- At MPS Target #1 AU$644m

- At MPS Target #2 AU$938m

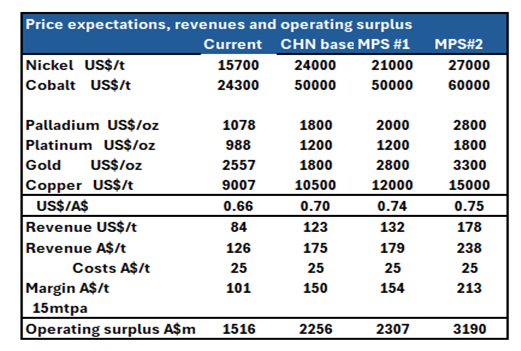

On the basis of a 15mtpa operation, the operating surplusses would be very large.

- At current prices AU$1,5168m

- At MPS Target #1 AU$2,307m

- At MPS Target #2 AU$3,190m

Exploration

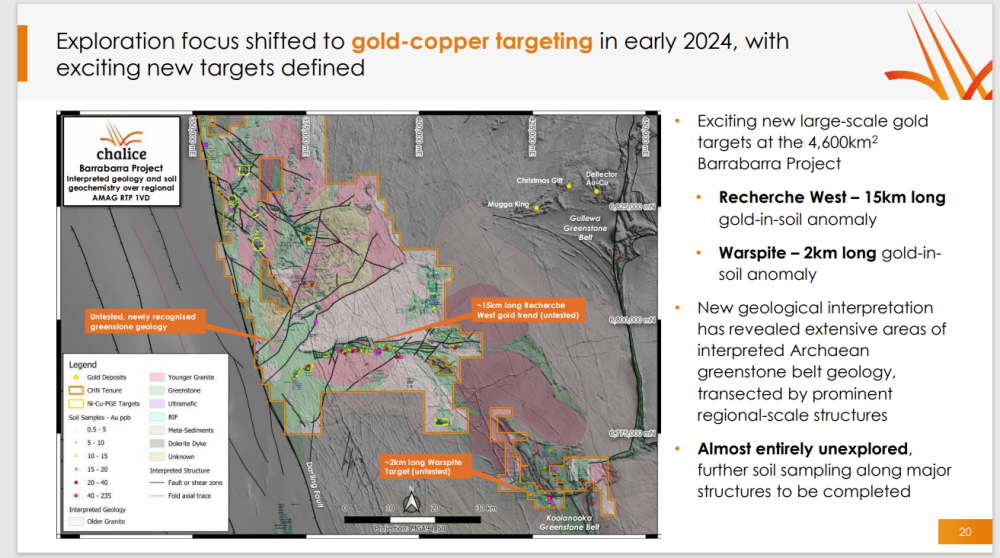

CHN has some very large exploration areas totaling ~10,000 km2 along 1200km of the West Yilgarn Province margin.

Chalice has identified >40 copper-gold and nickel-copper-PGE targets in this West Yilgarn province.

Note that much of this was undercover and mapped as `pink' granitic material, but CHN has found, as have ICL and NIM, much of the pink is actually mafic 'green' rocks.

Most of this area is completely unexplored.

Explorers are currently despised peasants, but over time, they will become kings. Keep in mind Tim Goyder's companies are very successful explorers.

No exploration, no deposits.

No deposits, no supply.

Higher prices are coming.

CHN is ready to recover lost ground.

Eventually, it will get back to previous highs and double thereafter.

Head the markets, not the commentators.

Important Disclosures:

- Barry Dawes: I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.