Squinting at the gold news from China, both official and private. . .

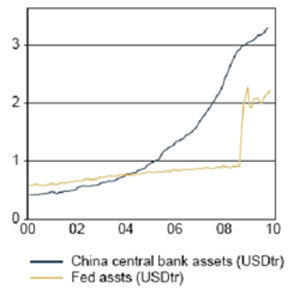

CHINA'S LATEST SLEW of positive data "raises the prospect" of Beijing tightening its easy money and fiscal policies, or so the newswires claim. Currency strategist Steven Barrow at Standard Bank adds that China could be more significant for global liquidity than the United States, too.

Because the Fed's asset pile is nothing next to the People's Bank's hoard of cash, he says. So "the Fed's grip on the [easy-money] punchbowl is not as firm as the market might think," as shown by Barrow's chart below.

The upshot for gold investors? Given that China's foreign reserves are at least 50% held in US Treasuries, dollars and government-backed agency bonds...and given that gold has risen four-fold vs. the greenback inside 10 years...and seeing how the gold market is currently spooked by a whiff of improving US data, and the tang of non-zero Dollar rates it might imply...it might be worth a look.

So let's squint through our telescope...10,000 miles distant.

Since the start of 2000, China's official gold reserves have grown by 167% to 1,054 tonnes, now the world's fifth largest central-bank hoard. That contrasts with the US Treasury sitting pat at 8,133 tonnes (the world's largest single hoard) and Western European banks selling around one-fifth of their "legacy" holdings so far this decade, (now down below 12,016 tonnes).

Beijing's style of reporting on gold also contrasts with Western announcements, made over the last 10 years within the precepts of the Central Bank Gold Agreement first signed in Sept. 1999 and renewed again this autumn. The CBGA sets a pre-declared sales ceiling of 400 tonnes per year, and also includes the International Monetary Fund's 403-tonne divestment (now half done thanks to the Reserve Bank of India buying 200 tonnes of IMF in October). Whereas the word "secretive" doesn't begin to describe China's official gold dealings.

The People's Bank only reports changes to its gold holdings occasionally and erratically. Pace the World Gold Council's numbers:

So on hearing the news, "China's announcement signals a broader shift in central banks' attitude towards gold," said Philip Klapwijk, chairman of the world-leading GFMS precious metals consultancy. "[This is] reigniting gold's relevance as a monetary asset," agreed Suki Cooper, gold analyst at Barclays Capital.

But was it really the big story? April's announcement took gold to around 1.6% of China's foreign currency reserves. Which was in fact lower than the 2003 level of 2%, courtesy of the seven-fold growth in China's foreign currency hoard. . .now around $2 trillion, up from $159bn at start-2000.

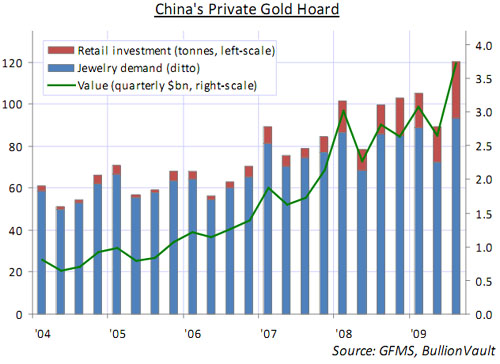

Bear that slippage in mind below. . .and bear in mind that the real Chinese demand story, both comparatively and across the global gold market, continues to be private consumption.

Basis the GFMS consultancy's data, Chinese households spent more on gold jewelry and physical investment during the third quarter of '09 than during all of full-year 2005. Spending a total of US$3.7 billion on the metal, Chinese consumers confirmed their world-beating demand for 2009-to-date, overtaking Indian households as the world's No.1 buyers.

Considering that jewelry taxes were only relaxed in 2002, and investment was allowed only from 2005, that's some move to now top the table, even for the world's most populous nation. And on our analysis here at BullionVault—based on World Bank estimates and GFMS figures—private mainland gold demand now equals some 2.0% of China's famously massive household savings, up from 1.0% ten years ago. . .and even as annual household savings have more than trebled.

Most critically, private mainland demand over the last five years has been almost four times what the People's Bank acquired from 2003–2009, piling up a massive 1775 tonnes in private hands. Cumulative buying rose 16% by value in the first 9 months of this year versus the same period in '08. But how much Beijing's easy-money and fiscal stimulus is to thank—rather than cultural trust in gold and quasi-religious auspicion, both polished by private wealth accumulation—who can say. . .?

(Adornment and investment motives, as an aside, are more difficult to separate in the East than here in the West. Hence the catch-all "investment jewelry" referred to by Wall Street and City analysts looking at Indian and Asian gold.)

Back at the People's Bank—which employs fewer staff per 100,000 of population than anyone else by the way, down at 0.19 compared to the Fed's 19.9 and Russia's staggering 71.2 according to the Economist this week—official opinion on gold is divided. What the European and North American financial pages typically see as a communist monolith in fact contains (and gives voice to) a diverse and often controversial set of views. But three aims seem clear:

Not quite. Because for central banks, gold is a politically-charged asset, not simply a portfolio hedge. "Germany in 1944 could buy materials during the war only with gold," as Alan Greenspan noted in 1999. "Fiat money in extremis is accepted by nobody." And look at the numbers Ji quoted—6,000 tonnes would take China way above Germany. 10,000 would trump Washington.

Gold is a safe haven for all investors because there is "no violation of contract" noted Zhang Bingnan, a senior member of the China Gold Association, to Reuters at the Shanghai Gold Conference last week. "Gold is the only non-credit product in the financial market." These attributes only stand out more clearly for central bank policy wonks and long-term planners hoping to keep control of the fastest-growing economy on earth.

Still, the People's Bank can't avoid T-bonds entirely, of course, even if it is cutting its agency holdings. There's simply not enough gold in the world, and too many Dollars, for that. That's why "We hate you guys," as Luo Ping, a director-general at the China Banking Regulatory Commission (CBRC) complained on a visit to New York in February.

"Once you start issuing $1-$2 trillion. . .we know the Dollar is going to depreciate, so we hate you guys, but there is nothing much we can do."

One thing Chinese officials can do—if they're to try and keep pace with private gold demand, and anchor the nation's money reserves with gold—is to buy directly from the minehead. That was how South Africa built its Forex reserves during apartheid sanctions in the late 20th century. Back then, South Africa was the world's No.1 mining producer. It just so happens that China is today.

"It's cheaper for us to buy gold from the Chinese market," said an un-named People's Bank official to Western journalists last month, "but it doesn't help diversify our huge foreign exchange reserves. Even if China bought half the world's annual gold supply, it would only cost a few tens of billions of dollars, which is tiny compared to China's huge reserves."

"Even if it's sold at a market price, we should still buy," counters Xia Bin, head of a key Beijing think tank advising the State Council cabinet (and also making plain that this is his personal view).

"India's okay with it, why shouldn't we be? What's the use for so many dollars, whose purchasing power is weakening anyway? With so many foreign reserves in hand, I think China should buy, without doubt."

Either way, "China has the scope to step up gold purchases but should take a long-term approach, avoiding the open market," says Zhang of the China Gold Association. "If we adopt a too aggressive and rash manner, it is not practical." Because China-inspired surges in the gold price would only work to make buying gold more expensive, as the recent case of India's 200-tonne purchase makes plain.

India's move was "probably the most remarkable event in the gold market since the Central Bank Gold Agreement (CBGA) was announced in late September 1999," according to Matt Turner at the VM Group. Glance at November's price chart and you've got to agree, at least short term. Gold cut a straight line from $1045 to $1226 an ounce.

Yes, it's come down sharply from there. But that's perfect for price-conscious consumers getting set for January's New Year celebrations. . .and it's just the thing for long-term strategic planners wanting to build their hoard.

Adrian Ash

BullionVault

Gold price chart, no delay | Gold in 2009

Formerly City correspondent for The Daily Reckoning in London and head of editorial at the UK's leading financial advisory for private investors, Adrian Ash is the editor of Gold News and head of research at BullionVault—winner of the Queen's Award for Enterprise Innovation, 2009—where you can Buy Gold Today vaulted in Zurich on $3 spreads and 0.8% dealing fees.

(c) BullionVault 2009

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events—and must be verified elsewhere—should you choose to act on it.

CHINA'S LATEST SLEW of positive data "raises the prospect" of Beijing tightening its easy money and fiscal policies, or so the newswires claim. Currency strategist Steven Barrow at Standard Bank adds that China could be more significant for global liquidity than the United States, too.

Because the Fed's asset pile is nothing next to the People's Bank's hoard of cash, he says. So "the Fed's grip on the [easy-money] punchbowl is not as firm as the market might think," as shown by Barrow's chart below.

The upshot for gold investors? Given that China's foreign reserves are at least 50% held in US Treasuries, dollars and government-backed agency bonds...and given that gold has risen four-fold vs. the greenback inside 10 years...and seeing how the gold market is currently spooked by a whiff of improving US data, and the tang of non-zero Dollar rates it might imply...it might be worth a look.

So let's squint through our telescope...10,000 miles distant.

Since the start of 2000, China's official gold reserves have grown by 167% to 1,054 tonnes, now the world's fifth largest central-bank hoard. That contrasts with the US Treasury sitting pat at 8,133 tonnes (the world's largest single hoard) and Western European banks selling around one-fifth of their "legacy" holdings so far this decade, (now down below 12,016 tonnes).

Beijing's style of reporting on gold also contrasts with Western announcements, made over the last 10 years within the precepts of the Central Bank Gold Agreement first signed in Sept. 1999 and renewed again this autumn. The CBGA sets a pre-declared sales ceiling of 400 tonnes per year, and also includes the International Monetary Fund's 403-tonne divestment (now half done thanks to the Reserve Bank of India buying 200 tonnes of IMF in October). Whereas the word "secretive" doesn't begin to describe China's official gold dealings.

The People's Bank only reports changes to its gold holdings occasionally and erratically. Pace the World Gold Council's numbers:

- In 1981 China had 395 tonnes;

- End-2001 that moved to 500.8 tonnes;

- End-2002 it rose to 600 tonnes;

- April 2009 saw China announce it held 1054 tonnes.

So on hearing the news, "China's announcement signals a broader shift in central banks' attitude towards gold," said Philip Klapwijk, chairman of the world-leading GFMS precious metals consultancy. "[This is] reigniting gold's relevance as a monetary asset," agreed Suki Cooper, gold analyst at Barclays Capital.

But was it really the big story? April's announcement took gold to around 1.6% of China's foreign currency reserves. Which was in fact lower than the 2003 level of 2%, courtesy of the seven-fold growth in China's foreign currency hoard. . .now around $2 trillion, up from $159bn at start-2000.

Bear that slippage in mind below. . .and bear in mind that the real Chinese demand story, both comparatively and across the global gold market, continues to be private consumption.

Basis the GFMS consultancy's data, Chinese households spent more on gold jewelry and physical investment during the third quarter of '09 than during all of full-year 2005. Spending a total of US$3.7 billion on the metal, Chinese consumers confirmed their world-beating demand for 2009-to-date, overtaking Indian households as the world's No.1 buyers.

Considering that jewelry taxes were only relaxed in 2002, and investment was allowed only from 2005, that's some move to now top the table, even for the world's most populous nation. And on our analysis here at BullionVault—based on World Bank estimates and GFMS figures—private mainland gold demand now equals some 2.0% of China's famously massive household savings, up from 1.0% ten years ago. . .and even as annual household savings have more than trebled.

Most critically, private mainland demand over the last five years has been almost four times what the People's Bank acquired from 2003–2009, piling up a massive 1775 tonnes in private hands. Cumulative buying rose 16% by value in the first 9 months of this year versus the same period in '08. But how much Beijing's easy-money and fiscal stimulus is to thank—rather than cultural trust in gold and quasi-religious auspicion, both polished by private wealth accumulation—who can say. . .?

(Adornment and investment motives, as an aside, are more difficult to separate in the East than here in the West. Hence the catch-all "investment jewelry" referred to by Wall Street and City analysts looking at Indian and Asian gold.)

Back at the People's Bank—which employs fewer staff per 100,000 of population than anyone else by the way, down at 0.19 compared to the Fed's 19.9 and Russia's staggering 71.2 according to the Economist this week—official opinion on gold is divided. What the European and North American financial pages typically see as a communist monolith in fact contains (and gives voice to) a diverse and often controversial set of views. But three aims seem clear:

- Diversification: Beijing's wonks don't need to read the Journal of Portfolio Management to know gold's quadrupled vs. USD, Yen, Sterling, CHF (and Yuan) and trebled vs. Euro since 2000;

- Domestic crowd-pleasing: See household demand above, and set next to the Reserve Bank of India buying 200 tonnes from the IMF. . .just as private Indian households slow their gold hoarding in the face of relentlessly higher prices;

- Economic prestige: The golden rule (He who has the gold, etc.) will suit even Beijing's longest long-term thinkers. The United States ended WWII with more than 21,000 tonnes of gold, some 70% of total monetary metal. Dollar rule came as a direct result. So if the Dollar's now toast, and power is truly shifting across the Pacific, the big picture would demand a big pile of bullion.

Not quite. Because for central banks, gold is a politically-charged asset, not simply a portfolio hedge. "Germany in 1944 could buy materials during the war only with gold," as Alan Greenspan noted in 1999. "Fiat money in extremis is accepted by nobody." And look at the numbers Ji quoted—6,000 tonnes would take China way above Germany. 10,000 would trump Washington.

Gold is a safe haven for all investors because there is "no violation of contract" noted Zhang Bingnan, a senior member of the China Gold Association, to Reuters at the Shanghai Gold Conference last week. "Gold is the only non-credit product in the financial market." These attributes only stand out more clearly for central bank policy wonks and long-term planners hoping to keep control of the fastest-growing economy on earth.

Still, the People's Bank can't avoid T-bonds entirely, of course, even if it is cutting its agency holdings. There's simply not enough gold in the world, and too many Dollars, for that. That's why "We hate you guys," as Luo Ping, a director-general at the China Banking Regulatory Commission (CBRC) complained on a visit to New York in February.

"Once you start issuing $1-$2 trillion. . .we know the Dollar is going to depreciate, so we hate you guys, but there is nothing much we can do."

One thing Chinese officials can do—if they're to try and keep pace with private gold demand, and anchor the nation's money reserves with gold—is to buy directly from the minehead. That was how South Africa built its Forex reserves during apartheid sanctions in the late 20th century. Back then, South Africa was the world's No.1 mining producer. It just so happens that China is today.

"It's cheaper for us to buy gold from the Chinese market," said an un-named People's Bank official to Western journalists last month, "but it doesn't help diversify our huge foreign exchange reserves. Even if China bought half the world's annual gold supply, it would only cost a few tens of billions of dollars, which is tiny compared to China's huge reserves."

"Even if it's sold at a market price, we should still buy," counters Xia Bin, head of a key Beijing think tank advising the State Council cabinet (and also making plain that this is his personal view).

"India's okay with it, why shouldn't we be? What's the use for so many dollars, whose purchasing power is weakening anyway? With so many foreign reserves in hand, I think China should buy, without doubt."

Either way, "China has the scope to step up gold purchases but should take a long-term approach, avoiding the open market," says Zhang of the China Gold Association. "If we adopt a too aggressive and rash manner, it is not practical." Because China-inspired surges in the gold price would only work to make buying gold more expensive, as the recent case of India's 200-tonne purchase makes plain.

India's move was "probably the most remarkable event in the gold market since the Central Bank Gold Agreement (CBGA) was announced in late September 1999," according to Matt Turner at the VM Group. Glance at November's price chart and you've got to agree, at least short term. Gold cut a straight line from $1045 to $1226 an ounce.

Yes, it's come down sharply from there. But that's perfect for price-conscious consumers getting set for January's New Year celebrations. . .and it's just the thing for long-term strategic planners wanting to build their hoard.

Adrian Ash

BullionVault

Gold price chart, no delay | Gold in 2009

Formerly City correspondent for The Daily Reckoning in London and head of editorial at the UK's leading financial advisory for private investors, Adrian Ash is the editor of Gold News and head of research at BullionVault—winner of the Queen's Award for Enterprise Innovation, 2009—where you can Buy Gold Today vaulted in Zurich on $3 spreads and 0.8% dealing fees.

(c) BullionVault 2009

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events—and must be verified elsewhere—should you choose to act on it.