The Gold Report: What is the state of the current global graphite market and what impact might Tesla's construction of a battery Gigafactory in the desert in Nevada have on future demand for the mineral?

Blair Way: Because graphite is used in many energy-related applications (including electric vehicles, Pebble Bed Nuclear Reactors, fuel cells, solar panels and electronics ranging from smartphones to laptops), it has been categorized as a critical, strategic mineral by several governments including the United States and Europe.

What does this really mean? At this point in time it means nothing—graphite is in oversupply and prices are low. However, if China decided to stop supplying graphite to the world, then the West would be in trouble. This is highly unlikely to ever happen. As far as the impact of the Tesla plant on the greater market, that's yet to be defined in detail, but it will create more demand for graphite, both natural and synthetic.

TGR: How big is the graphite market?

BW: The graphite market combined—the natural flake and synthetic market—is worth approximately $13 billion ($13B). Synthetic is 90% of that market, and natural flake graphite is 10%.

TGR: How big is the natural flake graphite market?

BW: The worldwide natural flake graphite market hovers around 1.1 million tons a year (1.1 Mtpa) of which 75% is from China, 11% from India, 6% from Brazil, 3% from North Korea and 5% from the rest of the world. Consumption of graphite is also approximately 1.1 Mtpa, and 65% is consumed in China. The balance of the production is consumed in Brazil and India (200,000 tons), with 100,000 tons in Europe and 100,000 tons in North America. Of this 1.1 Mtpa, more than 60% is fine and medium graphite while the balance of 40% is flake graphite. The majority of this flake graphite is micronized for the end user.

TGR: How important is it to understand the graphite market in terms of dollar value?

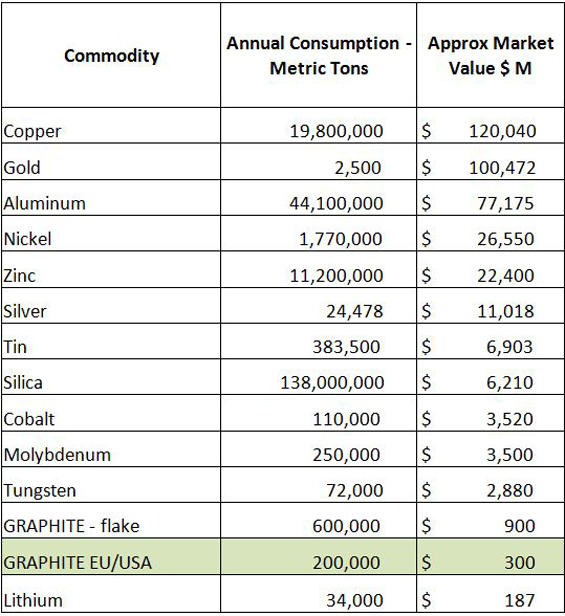

BW: World production and consumption of natural flake graphite is often claimed to be almost as large as the nickel market (1.8 Mtpa) by volume.

The market should be considered by dollar value not just tons per annum. As a comparison, the 1.1 Mtpa of graphite is worth $1.3B while 1.8 Mtpa of nickel is worth $26B. As a new entrant to the market, nickel is a significantly larger market than graphite. So to put the graphite market in perspective, the non-Chinese natural flake graphite market is a $300 million ($300M) market. This is the market in which all the Western graphite producers (current and future) are vying for position.

That is why a new graphite production facility must start small and build relationships in the current market while developing products that can supply the anticipated future markets. Cash flow for a graphite business must be sensible in today's market.

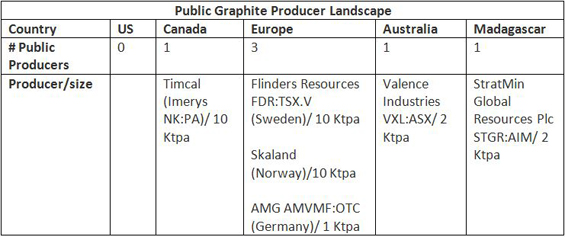

Chart provided by Flinders Resources

TGR:What is the size of a big graphite mine and what kind of revenue stream should investors expect from a natural flake graphite mine selling into the traditional market?

BW: A large graphite mine would be 10,000–20,000 tons per year (10–20 Ktpa) and would have a revenue stream of $10–20M. Profit could be in the range of $3–8M. This is similar in scale to a 10,000–20,000 ounce gold mine. Any graphite miner claiming a large-scale operation will not be able to achieve the sales as a new entrant to the market. It is possible that the mine could grow to a much larger size over time, but the sales must drive expansion of production. If too much concentrate is produced and it does not sell, then working capital will diminish quickly and the business will be in trouble.

TGR: What sort of revenue should you expect from a high-purity natural flake graphite miner selling into the battery market?

BW: High-purity natural flake graphite can and does displace some synthetic graphite. The market for synthetic graphite is about 1 Mtpa, which at prices of $5,000–10,000 per ton indicates a market size of $5–10B annually. Approximately 50% of the synthetic graphite produced is used for electrodes in the steel industry. The uses of synthetic graphite are varied, but for batteries the quantity of natural flake graphite consumed is less than 100 Ktpa. The synthetic graphite market is as private as the natural graphite market, so figures quoted can vary greatly. There are multiple new uses for high-purity graphite beyond conventional batteries, so there is huge potential for the growing market for high-purity natural flake graphite.

TGR: We often hear about the importance of offtake agreements. Can you explain to us the important distinction between offtake agreements and sales agreements?

BW: Offtake agreements are not sales agreements—they are non-binding agreements to purchase future production if a number of provisions are met. A sales agreement is a commitment to quantity and price per ton for a set period of time. Most junior mining companies are not signing sales agreements because graphite consumers want to lock in prices below known market prices.

To evaluate the offtakes you have to ask the questions: Did the buyer invest hard cash in the graphite business to facilitate the start of production? Does the contract with the buyer protect the producer or the buyer? Is there a guaranteed minimum or maximum price when the market price is constantly changing? Is there a minimum price in the agreement? Is it a take-or-pay agreement? What are the escape clauses for the buyer to get out of the agreement? Does the agreement cover all grades produced by the graphite producer, or is it just the grades the buyer requires? What happens to the products that the buyer is not interested in?

There is little to no hedging of graphite because it is not a publicly traded commodity, and it is very unlikely a trader will hedge for a producer. If a trader does offer to buy at a set price it would be at historically low prices. This will benefit the trader and not the producer. Typical refractory customers do not buy graphite in large enough quantities to justify locking in prices. They can also stockpile if required to ride out higher pricing. Even high graphite prices do not have a huge impact on overall pricing of the end product because graphite, by cost, is a small part of the cost of the products.

TGR: One of the buzzwords we hear when companies in the graphite space tell their story is "graphene" and the potential for their company to one day produce it. How important should graphene exposure be to an investor or speculator when deciding what companies in the graphite space to invest in?

BW: Graphene is 10–20 years away from being commercially viable, so one cannot justify a graphite mine based on the graphene market. The graphene market will take an extremely long time to develop products for everyday use. Additionally, a small amount of graphite goes a long way in making graphene.

There are two kinds of graphene. One is made from chemical vapor deposition, in which a graphene coating is made on top of another substrate, then the substrate is removed, leaving only the graphene. Most of the graphene being used today is made that way. That is the graphene the electronic industry wants because it's ultra-high purity and can be easily controlled.

Feeding the Mill. Photo provided by Flinders Resources

The lower-cost way uses natural graphite as the precursor. That market will take longer to develop, but it will be a bigger market because that kind of graphene can be used in the more practical, higher-volume products that we use every day. As a graphite producer, it is important to be part of the R&D process and to drive it towards commercialization. Flinders Resources Ltd. (FDR:TSX.V) is an active part of this R&D process supplying graphite to research facilities.

Graphene will not have positive impacts on a graphite producer's cash flow until commercialization has taken place and there is a real market for it. Graphene will be produced by specialists, not miners. Miners will supply the materials to enable graphene manufacturing.

TGR: What should be on an investor's checklist when considering a potential investment or speculation in the graphite space?

BW: Production of graphite is only one step to becoming a graphite producer. Sales must be secured to ensure all concentrate produced will sell. The market is a closed market and if sales are not secured for production, selling product is extremely difficult. Can the company sell its product at a profit?

There are four key elements to determine the quality of a graphite company:

1) Capital costs of the project:

Capital expenditures (capex) is a huge driver and this is what really kills a project–especially a low-revenue business like graphite. Consider many nickel laterite projects and how typically the first owner runs out of cash, and it is the second or even third owner that actually makes the business work. The capex kills the first owner almost every time. Aluminum is similar too. Both these commodities have a huge market to supply; graphite does not. The scale for graphite is much smaller, but the same elements of capex are at play.

2) Marketing/production rate:

Bigger is not better—except it is often required to justify high capex. The market does not support the mega graphite projects (anything over 10–20 Ktpa). If the company cannot make money at modest rates, the project will most likely fail. The marketing section of most feasibility studies to date do not have a credible source of information. If a gold project was to sign off its own marketing section of a feasibility study claiming to use an average selling price of gold at $2,000 per ounce, there would be an uproar. That is what appears to be happening in graphite for most studies.

There are no expert traders who can or will provide an independent opinion on the market for a particular project's product. If they did, it would not serve the project well. That is one of the reasons we approached the Woxna project in Sweden the way we have—to test the market in real time to be sure we understand it. You could never do this for a base metal or precious metal, but the scale of graphite is such you can and we have. Being a graphite producer and selling into the market means we know more than most about the market.

3) Operating cost (Opex):

Can the product be sold at a profit for all fractions of the production? Every deposit produces a mixed bag of concentrate with fine, medium and large flakes. The large flakes will naturally have the higher carbon content and the medium less and fine less again. The quantity of each will have a big impact on the average selling price. Sometimes the fines do not sell at all–or for very little. This can increase the cost of the higher value concentrate. All producers hoping to start up must have a high-purity strategy. They will not be profitable until they can value add all the concentrates.

4) Value adding the concentrate to increase margins:

Does the company have a credible high-purity strategy–a flow sheet defined and tested? Anyone can purify with a leaching plant or thermal, but it can be very costly. The flow sheet must not only prove technical success but also be economic. It must be less than $1,500/ton to produce to 99%+ carbon. This is rarely, if ever, discussed in the high-level, high-purity strategies. To ask a lab to confirm it can be done is almost worthless; the economics must be defined. All graphite samples can be purified to 99%+. The company must have done the work to define the economics and how to build and operate the high-purity plant. To discuss what purity can be achieved through flotation is a start, as the higher the carbon content feeding the HP plant, the lower the cost of the HP concentrate.

TGR: As an investor/speculator, what questions would you have for companies when evaluating their feasibility (FS) and preliminary feasibility study (PFS)?

BW: These are requirements under the NI 43-101 regulatory framework for all Toronto Stock Exchange-listed public companies. It is a requirement of greenfield projects to demonstrate technical and economic viability. A feasibility study is the final study before commencing detailed design and construction of the project, so it must include the permits to construct and operate the mine and facility. These studies are designed for large projects such as gold, copper, silver, nickel or zinc projects. Typically these are mines and processing facilities that cost hundreds of millions of dollars to build and generate revenues of hundreds of million dollars a year. A PFS can cost in excess of $5M and an FS can cost upwards of $10–20M for the most basic of projects.

When conducting a PFS or FS for a graphite project, these study costs are prohibitive. The revenue stream for the largest graphite mine in production today would be about $30M a year. This is the largest graphite mine in the world and it is located in China. The next largest mine is about 10 Ktpa, and that equates to a revenue stream of $10M a year. You will see many FS and PFS for graphite companies creating large revenue stream models as this is the only way to rationalize the capital costs to get these facilities in operation and build an impressive story for promotion. This is the challenge for graphite.

TGR: How relevant is the marketing component of a graphite study?

BW: In my opinion the marketing sections in the FS and PFS technical reports published by public companies are rubbish. There is no authority to go to for understanding the graphite business. There are a number of providers who publish reports on the graphite business, selling these reports for over $5,000, but the actual information on the market and actual buyers is minimal to non-existent. The reports are based on voluntary surveys sent to private businesses that are not obliged to supply accurate data, and in some cases it is beneficial to provide incorrect data.

The Woxna Processing Facility. Photo provided by Flinders Resources

These private organizations do not want their business to be known so they provide misinformation; the reports lack accurate data. Often the marketing sections of the studies published by graphite companies are signed off by insiders of the company. I have seen the marketing section signed off by the CEO—this is not independent and is highly biased. It is almost impossible to get real marketing information because the traders benefit by the confidential nature of the market. The commercial publications are paid-for publications, and they are not bound by any regulations to be reporting facts.

When you study these detailed reports on the production, which are also based on very poor information gathering techniques, and marketing you find limited detail on the actual end users and who buys the products and what they pay for it. This is due to the confidential nature of the graphite market. There is no way to accurately understand it without being in the business and selling product into the market.

TGR: Can you share some insight into what to look out for when interpreting metallurgical results?

BW: Many companies press release the results of bench scale or "pilot plant" test work and how they are achieving carbon contents as high as 97% or even 98% from flotation. These results are achievable in a full scale flotation plant but the engineering firm must have demonstrated experience in designing and building a graphite processing plant.

Another important point is the "pilot plants" purported to belong to the various companies claiming to have operated a pilot plant are actually modular plants constructed by a lab using the various components they have in inventory. This "pilot plant" is assembled using these components and then dismantled once the test is complete. This is not the same as many companies in other commodities that actually build small plants that test the flow sheet at reasonable scale on their sites. No graphite company has done this to date.

Flake size distribution in the lab-scale tests can vary quite significantly to the real-world, full-scale facility. Flotation of graphite is tricky. The natural flakes float best but as the feed is processed, more fine material is created during milling, and intermediate grinding impacts flake size distribution negatively. What this means is it is most likely that flotation will produce a mixed bag of flake sizes. Generally a 30–40% distribution of each fraction is expected. Each ore will perform slightly differently but there will always be a decent percentage of fine and medium flakes. The problem with this is that impurities also float into these medium and fines, which reduces carbon content to the low 90% range or even into the 80s for the fines. This results in a number of products when sorted into fine, medium and coarse and the associated carbon content of the fines in the mid-80s, mediums in the low 90s and large at 94%. The large flake is most valuable and the medium and fine will bring the average selling price down. It is unrealistic to expect to produce coarse, medium and fine concentrates all at 94%.

TGR: How important is flake size?

BW: Flake size is important primarily because during flotation the flakes liberate (float) most efficiently and these will yield the highest carbon content. As the flake size diminishes, typically the entrained impurities increase and the carbon content goes down. Customers specify large flake often to ensure they get the carbon content, even though they often grind or micronize the flake graphite for their processes.

Even spherical (SP) graphite, which often is thought must come from large flake, is misunderstood. SP is very fine graphite due to the mechanical process to create it. It must be natural flake graphite but it does not need to be large or even medium flake.

Some customers do require large flake sizes, but that is less significant than what is published in the industry. Carbon content is the most important factor in defining the value of the graphite concentrate. Some customers will pay a premium for micronized natural flake with high carbon content. The important issue is what fraction of the total concentrate product is high carbon content?

TGR: What are the flake size designations?

BW: Coarse, natural flake graphite is plus-50 mesh/300 μ, medium flake is plus-80 mesh/180 μ and fine flake is minus-80 mesh/180 μ.

TGR: How are prices for natural flake today?

BW: Prices are down for all natural flake graphite. This is due to the drop in demand, which is a direct result of the decline in the steel sector. Current medium to large flake 94% graphite is selling for less than $700 per ton and, in some cases, just not selling as there is a surplus of concentrate currently. Buyers are making low offers to producers to secure cheap concentrate for the future market.

TGR: How important is resource size?

BW: The resource size is not as important as many would like the public to believe. Graphite is not that rare so it is quite easy to find a large deposit that would deliver 10–20 years life of mine for a 10–20 Ktpa business. It is important to keep in mind the size of the graphite market when compared to the size of the resource. For example, 100% of the graphite market in Europe could be met by a resource of 1 Mt at 10% Cg. So 10 years and 100% European supply is 10Mt at 10% Cg. This is for 100% of the market which, of course, is unrealistic. A new entrant to a market would be lucky to get 10–20% market share. To identify hundreds of millions of tons of resource is not as valuable as is the case for base metals or precious metals.

TGR: How important is the grade of the resource?

BW: The resource grade is important primarily due to mining costs. The lower the grade, the more material that must be moved to produce a concentrate. Typically a lower grade deposit will be more costly to mine. Anything under 5% is a concern given that there are many graphite deposits in the world with higher grades.

TGR: When analyzing any deposit, we always look for the fatal flaw. What is really important in a graphite deposit?

BW: The location, configuration and metallurgy of the deposit are critical. The deposit must be near all key infrastructure, including sealed roads, inexpensive electricity, port facilities, and preferably an existing processing facility. To include the cost for roads, electricity or long transportation distances to port and customers in capex will severely impact a new graphite project. These three elements will have a significant negative impact on both capex and opex. Sunk cost on the infrastructure is the most cost effective way for a graphite business to establish itself. Equally important is access to a decent work force and skilled labor for maintaining the mine and processing facility.

The deposit must be easy to mine–high grade and low stripping ratios are critical. The metallurgy of the deposit is hardest to understand–who is actually testing the deposit? Have they ever designed an operating graphite plant? What experience is there to actually assess the metallurgy and design an efficient full scale flow sheet?

TGR: How do you purify natural flake graphite? Do you use a chemical leach or thermal?

BW: Leaching is the chemical breaking down of impurities in a flotation concentrate and typically uses hydrofluoric, hydrochloric and sulphuric acid as a minimum to achieve the high-purity concentrations. These acids must be used to consume the impurities that cannot be removed by flotation. This can be costly and the cost per ton of 99.9% concentrate can range from $500–3,000/ton, depending on concentrate feed carbon content, mineralogical compositions, operation conditions, permitting requirements and availability of acids.

Thermal purification is simply the heating of a concentrate in a special oven to 3,000 to 4,000˚ C to burn off all impurities. This is simpler but generally more costly because of the high energy requirements to heat the concentrate. The costs of this can vary from $1,500–10,000/ton, depending on energy cost.

TGR: Where does Flinders fit in the graphite mining landscape?

BW: Flinders Resources is the only Western public company with a permitted, fully operational modern mine and production facility able to produce natural flake graphite and is in a strong position to place itself as a supplier of choice for the rapidly expanding and game changing lithium-ion battery energy storage.

The company has been working on optimizing a flow sheet to produce high-purity graphite that was substantially developed in the early 2000s by the previous owner of the Woxna project. We are negotiating with existing high-purity technological providers.

Flinders has a market cap of less than CA$10M; CA$4M is backed by cash. With a fully constructed, permitted and producing plant and mine, zero debt and cash on hand, the company is well positioned to leverage its first-mover advantage to concentrate its resources on research to produce high-purity grade graphite and initiate the relevant permitting.

TGR: Thank you, Blair, for your time.

Chart provided by Flinders Resources

Blair Way, CEO, president and director of Flinders Resources, has over 25 years of management experience within the resources and construction industry throughout Australasia, Canada, the United States and the United Kingdom. Prior to joining Flinders Resources Way was vice president of project development for Ventana Gold (Vancouver), advancing projects in Colombia. Way also previously served as president and project director for OceanaGold Philippines, project manager with Hatch Associates (Brisbane) and project director for BHP's Major Projects division (QNI Pty Ltd) in Townsville, Queensland. Way holds a Bachelor of Science in geology from Acadia University in Nova Scotia, Canada, a Masters of Business Administration from the University of Queensland, Australia, and is a Fellow of the Australasian Institute of Mining and Metallurgy.

DISCLOSURE:

1) JT Long edited this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the following companies mentioned in this interview: None.

2) Flinders Resources is a banner advertiser on Streetwise Reports.

3) Blair Way had final approval of the content and is wholly responsible for the validity of the statements which are believed to be true as at the date provided, based on information currently available to Mr. Way and any statements or opinions made by Mr. Way are an expression of opinion only and for information purposes only. This interview is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, province, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction. This interview does not constitute or form a part of, and should not be construed as a recommendation, offer, solicitation or invitation to subscribe for, underwrite or otherwise acquire securities in any jurisdiction. Readers are encouraged to do further research or seek advice from qualified advisors. Information contained in this interview contains forward looking statements which are subject to a number of factors, risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements, including, among other things, Flinders has yet to generate a profit from its activities; there can be no guarantee that the estimates of quantities or qualities of minerals disclosed in Flinders' public record will be economically recoverable; uncertainties relating to the availability and costs of financing needed in the future; competition with other companies within the mining industry; the success of Flinders is largely dependent upon the performance of its directors and officers and Flinders' ability to attract and train key personnel; changes in world metal markets and equity markets beyond Flinders' control; mineral reserves are, in the large part, estimates and no assurance can be given that the anticipated tonnages and grades will be achieved or that the indicated level of recovery will be realized; production rates and capital and other costs may vary significantly from estimates; the Company's preliminary economic assessment is no longer current or valid and the Company has no plans to complete a new preliminary economic assessment, a pre-feasibility or feasibility study on the project, as a result there is an increased risk of technical and economic failure for the Woxna graphite project; unexpected geological conditions; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; all phases of a mining business present environmental and safety risks and hazards and are subject to environmental and safety regulation, and rehabilitation and restitution costs; Flinders does not maintain insurance against environmental risks; and management of Flinders have experience in mineral exploration but may lack all or some of the necessary technical training and experience to successfully develop and operate a mine. Although Mr. Way believes that the expectations reflected in the Forward-Looking Statements, and the assumptions on which such Forward-Looking Statements are made, are reasonable, there can be no assurance that such expectations will prove to be correct. Readers are cautioned not to place undue reliance on Forward-Looking Statements, as there can be no assurance that the plans, intentions or expectations upon which the Forward-Looking Statements are based will occur. Forward-Looking Statements herein are made as at the date hereof, and unless otherwise required by law, neither Flinders nor Mr. Way intend, or assume any obligation, to update these Forward-Looking Statements.

4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.