In our Nov. 11 Exploration Insights letter (see excerpt below) we discussed the dismal state of the junior mining sector. Today we will expand on this theme, looking at the state of the larger gold miners and the obstacles they face going forward. The objective is to lay out an investment thesis premised on mining and exploration trends that indicate we are entering a rather unique and potentially very profitable period of time in the junior mining sector.

From EI Nov. 11:

"Nevertheless, money for exploration will remain tight for anyone that cannot demonstrate a potentially significant success. A persistent theme from many of the companies at the various resource conferences I attend is: 'When the markets pick up in January we will finance'.

I doubt it."

Conversations with a number of companies at the reasonably well-attended San Francisco Hard Assets show reaffirm our previous observations—there will be a very long line of micro-cap juniors desperately seeking money early next year. I don't think it will turn out well for most, and suspect that next year's junior company exploration and wine cellar expenditures are going to be severely curtailed. A further observation from the San Francisco and New Orleans shows was that those companies with just enough cash to survive next year will be doing little more than making property payments while their geologists sit on their hands, "looking for an opportunity."

Consider: It costs in the order of $100,000 ($100K) just to cover the public company filing fees, pay for the financial audits, and share an office and phone line. If you have a secretary, president, and geologist on staff you're looking at around $400K a year minimum. Add to that, property payments, a few field trips, and samples and you're nearing $800K.

Drilling and serious work using consultants or staff puts your junior company over the $1 million ($1M) mark just to do a little work on a long shot exploration property. Based on data collected and published by John Kaiser, about 50% of the Venture-listed companies will fall into the category of being unable to cover basic costs, while another 20% can't afford to explore. As of September filings, there are over 600 junior explorers with less than $200K in the bank! Welcome to the land of the walking dead.

Accordingly, grassroots exploration by the juniors will be virtually dead next year (tough to raise money on concepts and soil anomalies) and aggressive drilling will be seriously curtailed (tough to raise money if you miss). Frontier regions like the Yukon and Colombia will be empty compared to the previous three years, with much of the ground coming free (expensive to explore and keep up property payments). Worse, the industry's only real hope for new large discoveries, deep and blind targets, are for the most part not going to be tested by the juniors because of the high cost and even higher risk ("technically encouraging" results are tough to sell). Discovery takes time, patience and money; all of which will be in short supply next year.

This all bodes ill for the major gold miners that desperately need new large and economic deposits and have been increasingly relying on the juniors to supply them.

Here's why:

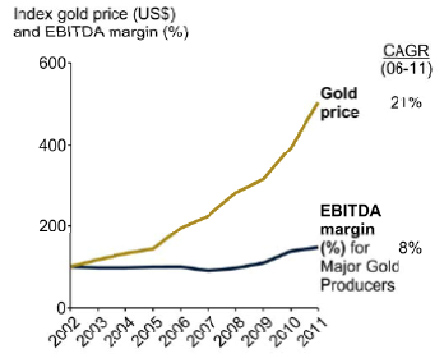

Since 2006, major gold equities have significantly underperformed gold bullion. The primary reason for the underperformance is that, despite the ~20% annualized increase in the gold price, major producers have only seen an 8% annualized margin growth since 2002 (Fig. 1 below). This equity underperformance has left many institutional investors who got the gold price investment thesis right sorely disappointed in the mining sector and recognizing it for what it is—a lousy business. They are unlikely to pile back into the miners; hence the high valuations for royalty companies whose exposure to cost pressure is less.

(Fig. 1: EBITA margins of six major producers compared to annualized gold price increase. From Nick Holland, CEO Gold Fields Ltd. Melbourne Mining Club; available here.)

The reasons for the poor economic performances are many and, to some degree, company specific; overall, however, it comes down to mining costs (which have shown an annualized increase of 32%), and the declining quality of gold deposits.

Exploration, development and sustaining capital costs have gone through the roof, resulting in a number of gold deposits being put back on the "maybe someday" shelf and out of the economic reserve category. Recent examples include Barrick Gold's decision to hold off on the development of 19 million ounces (Moz) at Donlin Creek and 17 Moz at Cerro Casale because they "do not meet investment criteria." Just this month, Gold Fields also pulled plans for open pit development of its 7.5-Moz Chucapaca deposit due to high capital costs. Even smaller deposits like Richmont's ~2.5 Moz (Measured Indicated and Inferred) Wasamac gold deposit has been pulled because "it generated a less than adequate return" following the results of a number of optimization studies. I suspect there are many more large- and small-scale projects to be pulled; companies want to avoid the dilemma Barrick faces at Pascua Llama--an initial $3.5 billon ($3.5B) capex estimate is now over $8B, with no turning back.

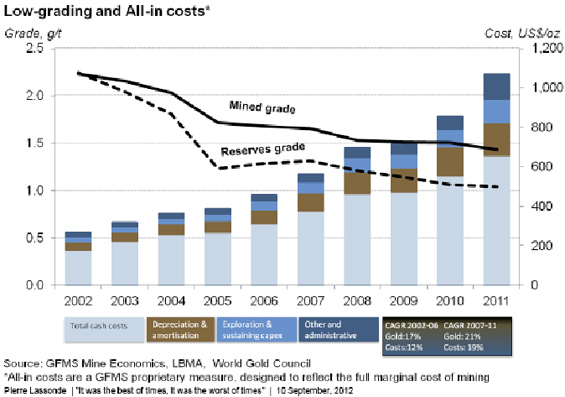

Total industry cash production costs have increased since 2002, from about $200 to nearly $700 per ounce (oz) (Fig. 2 below), while all-in costs are between $1,100/oz and $1,500/oz (depending on your source). Over the same period, the average mined grade of deposits has fallen by about half, while the mine reserve grade is projected to be only about 1 gram per tonne (g/t) this year: a 60% drop in 10 years.

(Fig. 2: Gold mining costs and grade, 2002 to 2011. Video link to Denver Gold Group presentation here).

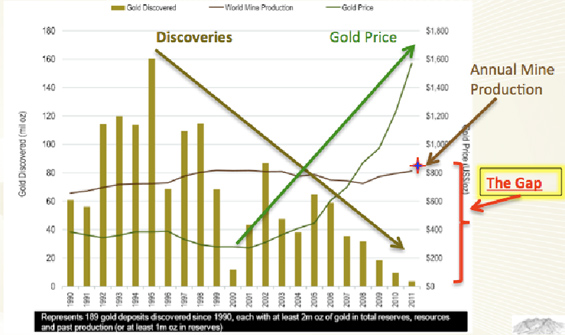

The declining mined and mineable gold grade is a direct result of the industry's inability to discover new high grade/high margin deposits. This lack of discovery has required companies to go after the lower grade/lower margin material around their current mines, using the increasing gold price to "find" the new ore. In fact, the Metals Economic Group estimates that the 99 significant discoveries (defined as greater than 2 Moz) found between 1997 and 2011 could replace only 56% of the gold mined during that same period. Further, these discoveries only account for 18% of the reserves and resources in the current producing and development stage projects, again demonstrating the dearth of new deposits.

This can't go on forever, and how the gap between current mine production of ~83 Moz and the rapidly declining discovered economic ounces plays out is going to be really interesting and profitable to those of us in the discovery game (Fig. 3).

(Fig. 3: Gold discoveries, production, and the gold price 1990 to 2011. The "gap" represents a serious discovery deficit. [Extracted from my recent San Francisco Hard Assets presentation] Source, Metals Economic Group)

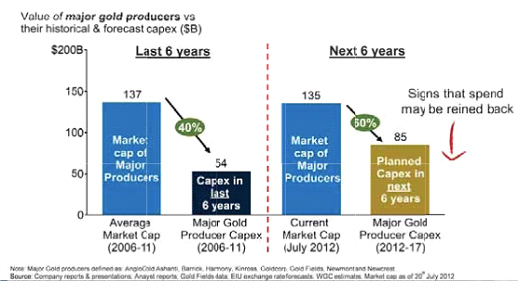

Another interesting data point to ponder when considering the 83 Moz of annual mine production, is how much it really costs the industry to maintain that production. Over the last six years, the major gold producers have spent 40% of their entire market capitalization building new mines (Fig. 4). In order to sustain that level of production going forward, published capex estimates project that the major miners will need to spend 60% of their market capitalization building the new mines, at a cost of $400B—and that figure doesn't even account for the nearly universal capex blowout we have witnessed over the past six years. Ouch!

(Fig. 4: Six major producers' market cap and capex—past six years and projected six years)

The Bottom Line

The major gold producers desperately need new, quality gold deposits yet can't afford to build many of the large deposits they already have on the books. These companies are facing margin squeeze in the form of increasing production and capital costs, taxes, royalties, regulations, etc., and are responding by cutting exploration, firing geologists and cancelling projects. That is a tough and illogical way to find new deposits.

As for the junior exploration sector, it is in the midst of one of the worst financing environments I have seen and, unless things change drastically over the next six months, faces mass extinctions. Without a new infusion of cash into the sector we will see much less work (exploration) of substance and far too many companies just covering expenses and business lunches.

These situations exacerbate the economic discovery deficit problem the gold industry faces. Therefore, and this is a not a revelation to long-time readers of Exploration Insights, the very few companies that have high quality gold deposits should be in more and more demand as this story plays out. Likewise, any exploration company with the property, competence, and cash to discover and define a quality deposit will be in even greater demand, due to the discovery leverage they offer. Conversely, a company with no cash and no property success means no more money and successively lower financings as they head off to the bone yard.

There are currently many junior mining stocks that are, or at least appear, "cheap" scattered across the decimated venture landscape. They could get much cheaper. How one measures cheap, however, had better be relevant to the real issues at hand: underlying value and quality as opposed to last year's share price or the price one paid. Specifically these are some of the questions that need to be addressed when considering "cheap."

- What is the realistic size and grade potential of the exploration target? Put another way: Is the target worth the effort?

- What are the probable mining, processing and capital costs if a deposit begins to be defined?

- What is the most likely metallurgy and recovery for the deposit type?

- How are social, environmental, permitting and political issues being addressed?

- What project goals and hurdles need to be reached to confirm the investment thesis, and at what cost?

- When and how does the company raise the money to advance the project and at what price?

- And the most obvious question: How far will the money it has have get the company?

Thus, at this juncture it is critical to review your stock holdings in the light of what could prove to be a very difficult period in the resource sector, yet one that offers exceptional opportunity when value is eventually realized sometime down the road. Significant economic deposits have been defined or will be discovered, and mining companies desperate to replace reserves and decrease overall costs will acquire them. There is no second option.

My experience has been that during bear markets like today's, one can often recognize and purchase deposits at a steep discount while the market wallows in self-pity. This is when tenbaggers are bought; but you had better know the value behind the deposits because there isn't much dumb money left to buy mistakes.

That's the way I see it.

Brent Cook, Economic Geologist and Editor of Exploration Insights

www.explorationinsights.com

Disclaimer

This letter/article is not intended to meet your specific individual investment needs and it is not tailored to your personal financial situation. Nothing contained herein constitutes, is intended, or deemed to be—either implied or otherwise—investment advice. This letter/article reflects the personal views and opinions of Brent Cook and that is all it purports to be. While the information herein is believed to be accurate and reliable it is not guaranteed or implied to be so. The information herein may not be complete or correct; it is provided in good faith but without any legal responsibility or obligation to provide future updates. Research that was commissioned and paid for by private, institutional clients are deemed to be outside the scope of the newsletter and certain companies that may be discussed in the newsletter could have been the subject of such private research projects done on behalf of private institutional clients. Neither Brent Cook, nor anyone else, accepts any responsibility, or assumes any liability, whatsoever, for any direct, indirect or consequential loss arising from the use of the information in this letter/article. The information contained herein is subject to change without notice, may become outdated and may not be updated. The opinions are both time and market sensitive. Brent Cook, entities that he controls, family, friends, employees, associates, and others may have positions in securities mentioned, or discussed, in this letter/article. While every attempt is made to avoid conflicts of interest, such conflicts do arise from time to time. Whenever a conflict of interest arises, every attempt is made to resolve such conflict in the best possible interest of all parties, but you should not assume that your interest would be placed ahead of anyone else's interest in the event of a conflict of interest. No part of this letter/article may be reproduced, copied, emailed, faxed, or distributed (in any form) without the express written permission of Brent Cook. Everything contained herein is subject to international copyright protection.