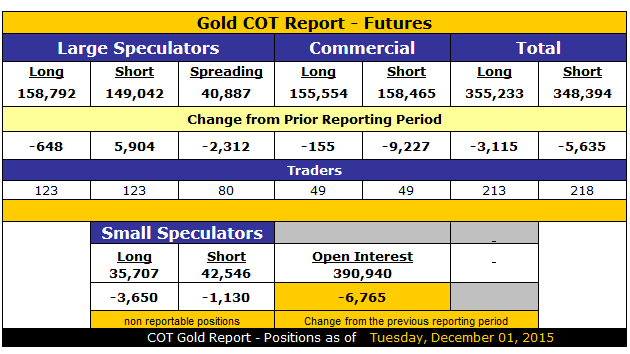

I have a question: "Does ANYONE have the foggiest recollection of just how incredibly bullish the Gold COT (Commitment of Traders) Report structure was back on Dec. 1, 2015?"

The Large Speculators were net long a paltry 9,750 gold futures contracts; today they are net long 285,911 contracts.

The Commercials were net short 2,911 contracts; today they are net short 315,477 contracts.

The always-wrong Small Speculators were net short 6,839 contracts; today they are net long 1,577 contracts.

Market timers for gold were 104% bearish (meaning that they were short); today they are 94% bullish (long to the teeth).

Gold miners were trading at valuations never before recorded; seven months later they are up 250%.

On December 1, 2015, gold was trading around $1,050/oz; today it is at $1,323/oz.

Now I have a second question: "Does anyone realize how things have changed?"

The COT Report shown below, while historically bearish, is not going to cause a crash in gold and silver prices; it is instead going to prevent a runaway in prices until the criminally inclined bullion banks have unwound what was two weeks ago a painfully acute paper loss in the billions. I only mention these two COT reports to illustrate the contrasts between then and now.

Despite the modest weekly improvement in the COT structure, gold and silver miners are trading down from the post-Brexit peak and have now given up the uptrend line that dates back until the January lows. Now, if the HUI (NYSE Arca Gold BUGS Index) can get back above the line sooner rather than later, it is a "no harm, no foul" scenario and 300–325 could be in the cards. My bet, however, is that the miners continue under pressure until July 31–August 15, and that there will be a downward trajectory that will allow for the bullion bank behemoths to unwind their massive short positions in paper-based gold and silver futures that are supposed to represent the actual physical metals but in reality are nothing more than synthetic proxies easily fabricated and used as weapons of mass abuse and distortion.

The gold and silver markets have completed a remarkable transition from the "most reviled sector in market history" (December 2015) to "There ain't no fever like GOLD fever!" here in July 2016. The Bay Street brokers are all falling all over themselves with gold and silver deals and my phone is ringing constantly with calls from prospectors and junior mining execs trying desperately to peddle their wares. Seven months ago, you could have picked up entire companies with decent portfolios of properties and prospects by just paying for their audited financials and exchange fees. My point is that as much as I love the rebound, it has gotten too crazy, too quickly, and with too many late arrivals now clamoring for positioning.

That is not to suggest that anything in my intermediate and long-term strategy has changed; I see gold through $1,425/oz and silver approaching $30/oz by year-end as the intermediate-term forecast I laid out in March kicks in. However, the short-term outlook will do precisely what our dear departed Richard Russell used to say about being "thrown from the horse" just as it takes off into flight. In my world, the unexpected appearance of a gut-wrenching, face-ripping correction in the metals would do what powerful bull markets do—punish the late arrivals and reward the early birds.

There is a certain portfolio manager often seen on Canada's Business News Network that was notoriously bearish on gold back in December, launching into this laborious explanation of why gold was doomed and headed to $700/oz: "We are in a deflationary period and there is no need to hold gold when prices are going down. Fluh-flah, fluh-flah-flah-fluf-fell…" It drove me bleeding-well bonkers to listen to this "wealth advisor" talking such utter nonsense (with the public actually BELIEVING him) so you can imagine my shock when I read a commentary from said "wealth advisor" last week that was urging clients to climb aboard the "precious metals train."

On the one hand, it frightens me when these trend followers finally capitulate and dive into the HUI 250% off the January lows; on the other hand, it is exactly what many of us have been predicting for many months. To wit, the number of portfolio managers actually recommending and owning gold and silver and the miners is estimated to be less than 1%. If that number were to grow to just 2% in the next year, I would hazard a guess that gold would see $2,400-2,500/oz with silver at $70/oz and the HUI at 500.

Interestingly, on a comparative basis, with the TSX Venture Exchange (TSX.V) ahead 68% from the January lows, it still remains moribund relative to the HUI (up 250%) or the GDX (Market Vectors Gold Miners ETF)—up 253%—or GDXJ (Market Vectors Junior Gold Miners ETF)—up 276%. Before this bull is over, the TSX.V is going to hit record highs and that record high was back in 2007 at 3,307, making the lift from current levels over 400%. When one uses the phrase "There ain't no fever like gold fever," it is important to understand that demographics have undergone an enormous shift as many of the prominent players from the big advance in the 1970s have passed on and the same is true for the big exploration decades of the 1980s and 1990s when new discoveries drove the markets.

What is noteworthy is that many of the new generation of investment bankers and traders are neither trained nor skilled in the intricacies of the exploration-driven TSX.V and as such have been largely avoiding it. That, my friends, is changing and when these new "Young Centurions," with their skills in social media and technology, discover the insane profit opportunities associated with a big, new, gold discovery, the TSX.V will be the focus of generations of inherited wealth, as well as decades of central bank currency debasement with the resultant miniscule market cap of the TSX.V moving up several orders of magnitude from current levels.

I cite as proof a recent interview with Goldcorp Inc.'s (G:TSX; GG:NYSE) Brent Bergeron being asked about his company's future M&A plans: "There are quite a few projects that are adjacent to Coffee, and we're always looking at possibilities that will allow us to build a camp and be here for the long term," Bergeron hints. "We're definitely watching what junior explorers are doing, and when it's appropriate we will make those investments and work with them to develop these opportunities. We want to make sure when there are promising projects that we're investing in moving them forward."

He was, of course, referring to Goldcorp's recent acquisition of Kaminak Gold Corp. for over $500 million and subsequent purchase of 19.9% of Yukon explorer Independence Gold Corp. (IGO:TSX.V) by way of private placement. These remarks represent a huge testimonial to the outlook for gold, for the Yukon, and for the White Gold District, and with Goldcorp's renowned skills in handling First Nations issues and permitting roadblocks, the path they are today blazing will be well used by the juniors in the region.

The top pick in my portfolio from 2015 was in fact Kaminak, which I tendered to the bid by Goldcorp (and subsequently hedged) but I still believe that the White Gold District will develop into a "camp" not unlike Timmins or Kirkland Lake or Rouyn with multiple major mines and associated infrastructure. Goldcorp's proposed road to Dawson City will reduce the seasonality for anyone with proximity to it so undoubtedly the fact that it will transverse the eastern portion of Stakeholder Gold Corp.'s (SRC:TSX.V) Ballarat project is a huge bonus for this little junior.

Stakeholder has completed Phase One of the 2016 exploration program (soils and GT probe [trenching]) and will soon begin 25 RAB drill holes designed to probe down to 100 meters in the areas covered by the soil grid. It must be noted that 2012 trench results yielded gold values greater than those found on the Coffee project so my hopes are quite high that those elevated levels of arsenopyrite and antimony are pathfinders to a large epithermal system. Results are expected in very early August. At a $6.6 million market cap, this micro-cap junior is a low-risk entry point for what we are all hoping will be Kaminak's little (or big) brother. (And please read the disclaimer at the conclusion of this missive.)

This week is going to prove to be critical for those looking for a near-term pop in the precious metals prices because we are getting a barrage of macro data and geopolitical noise all at once along with the Democratic National Convention or "DNC" but with recent allegations coming in from Wikileaks that some of the Hillary lieutenants were sabotaging Bernie Sanders during the primaries cannot be a positive for her. In fact, "DNC" might really stand for "Don't Need Clinton" as the Gong Show starts to heat up.

All I know is that we have finally relocated outside of the City of Toronto and further outside of the "GTA" (Greater Toronto Area, which includes the suburbs) to a small rural town to the northeast called Port Perry. It is about 20 minutes of additional commuting time to get to Bay and Wellington but the traffic is manageable and the air one breathes is superb. It reminds me of the little town where I grew up 55 years ago where you didn't lock your doors at night because the police force was comprised of 3,000 moms and dads with soup ladles and belts as "weapons." It was a different time and a different social psyche to be raised in the 1950s and 1960s, but the farther one moves from the "big cities," the more one feels as though they just got out of a time machine.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) The following companies mentioned in the article are sponsors of Streetwise Reports: None. The companies mentioned in this article were not involved in any aspect of the article preparation or editing. Streetwise Reports does not accept stock in exchange for its services. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

2) Michael Ballanger: I or my family own shares of the following companies mentioned in this article: Stakeholder Gold Corp. I personally am or my family is paid by the following companies mentioned in this article: Stakeholder Gold Corp. I am engaged as a consultant to Stakeholder Gold Corp. and am chairman of the Advisory Committee. I determined which companies would be included in this article based on my research and understanding of the sector.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

All charts and images courtesy of Michael Ballanger.