The name of this newsletter — The GGM Advisory — was derived from a weekly note that I invented while in the investment business from 1977 until 2014, which I called "Gold and Gold Miners." It all started in the midst of the 1981-1982 bear market that arrived on the heels of the Great Inflation of the 1970s, and it started out as a very bad idea as gold prices were well into a secular decline that lasted from 1980 until 2001.

Having followed gold throughout the 1970s, I used to buy copies of the Wall Street Journal every Saturday in order to get quotes for gold and silver while riding a bus between cities in the old Southern Hockey League.

In 1981, I was given a stock "tip" by a colleague who had friends in Timmins, a small northern Ontario town famous for its mines and hockey players. The Hemlo discovery of 1981 was directly responsible for my sojourn into the world of resource exploration and development, not only sparing my clients (and me) the agony of that bear market but also allowing me to meet some of the most fascinating entrepreneurs on the planet. (That is a topic for another day.)

If there was one enormous life lesson and career benefit, following the gold market meant I was forced to learn of its history dating back to ancient civilizations as it evolved through history. For centuries, the gold standard was the only governor preventing the banco-politico class from debasing the savings of its citizenry by profligate money-printing and debt creation. That all ended in 1971 when then-President Nixon tossed out the Bretton Woods Accord and eliminated the convertibility of U.S. currency into gold as a response to French President Charles De Gaulle insisting upon taking gold in lieu of currency when U.S. bonds bought by the French central bank began to mature.

The gold at Fort Knox was rapidly leaving the vaults as deficits caused by the guns-and-butter fiscal policies of the "Great Society" Johnson Administration and Viet Nam expenditures frightened foreign bondholders out of U.S. dollar investments. Closing the gold "window" kick-started a regime of unabated deficit spending and massive budget imbalances that, save for a very brief period during the Clinton years, has resulted in deficits and debt levels growing into today's out-of-control monstrosity.

This week we saw the price of gold advance through $2,700 per ounce settling out at a spot price of $2,720 and now resides a mere $30/ounce beneath the target price I set back in 2023. Inflows into the SPDR Gold Shares ETF (GLD:NYSE) exploded after experiencing net outflows during most of the past five years and look poised to accelerate.

This is a testimonial to the recent 180° shift in Wall Street attitudes toward gold and gold miners, and it can be best seen in the Kitco headline, which confirms the arrival of the generalist funds to that very foreign condition of gold ownership. These funds, which held gold allocations as high as 5% back in the 1970s, have been largely absent, with zero allocations to anything vaguely related to precious metals. I have been speculating for years on the possible outcome once these gargantuan funds turned to gold ownership, and now we are just beginning to see what 16 years of unbridled currency debasement has created as trillions upon trillions of newly-printed currency units around the globe are reallocated to gold and silver and the miners.

I have had an inordinate volume of emails and texts with queries, all asking what one should expect now that Wall Street and the public at large have rediscovered gold and silver. At first glance, the gold bugs are all now dancing in the streets as volume-starved miners welcome the arrival of liquidity and funding opportunities largely absent since 2020.

Conversely, Wall Street is always "late to the party" when it comes to niche investment narratives. For example, they pushed hard to get the Bitcoin ETFs approved by regulators, and once they got it, it was literally days before Bitcoin put in a top above $73,500. I fear that the arrival of the CNBC cheerleaders into the precious metals arena may be a similar event.

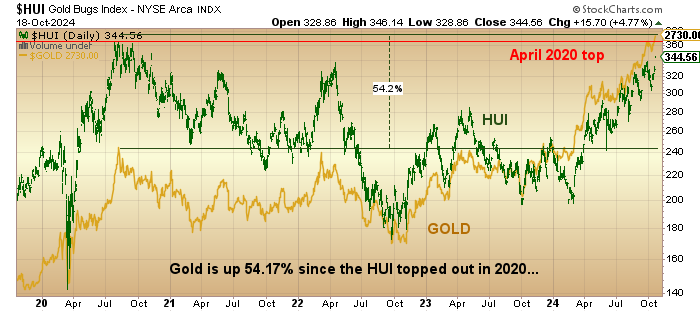

The chart shown above paints a far more optimistic picture, as it was over four and a half years ago that the NYSE ARCA Gold Bugs Index (HUI:US) topped out above 360, with gold trading at around $2,040. Here we are with gold, 54.2% higher since that date, yet the HUI has not even surpassed the old high. Keep in mind that the HUI topped out over thirteen years ago at over 620 with gold at $1,780, so to say that the miners have a great deal of "catching up" to do is an understatement of the highest order.

If I had to wager a guess, I would say that silver has even more "catching up" to do than gold, but of all the various categories of gold and silver investment, it is the junior developers, both gold and silver, that contain the greatest leverage to this continental shift in sentiment. This group has been orphaned for the better part of the past thirteen years and has been unable to mirror the performance and popularity of the group in the 1990s. I predict that we will see a return to the mania of the 1990s within the current cycle.

Near-term, using the GLD as a guide post, the market is now overbought albeit mildly, with MACD bearish but very close to a bullish crossover. Money flow indicators have been in decline but staged a late-week reversal that may constitute a bullish one. TRIX (a longer-term indicator) remains bearish.

Sentiment has certainly shifted, with the Bullish Percent Index now approaching the critical 90% level, which would constitute a "sell signal" once crossed.

All in all, I favor the miners over the physical right now because they are lagging the metal prices by such a wide margin, and I favor the juniors over the seniors, but by the term "juniors," I am not referring to the VanEck Junior Gold Miner ETF (GDXJ:NYSEArca) because it has very few (if any) non-producing developers included in its list of holdings.

I am referring to those juniors with defined resources or new discoveries (that are in the process of being quantified) because that is where the leverage truly resides. (Subscribers know the ones I like, so if you want the short list of junior developers, contact me.)

Silver

The silver bulls are finally achieving Nirvana as the all-important $33.50 level basis December futures was surpassed on Friday's huge advance, giving way to the possibility of an extended period of catch-up, which would entail the GSR (gold-to-silver ratio) dropping from the current 80.80 to the mid-50's. I have been cautiously bullish on silver only in the past two months, primarily due to the terrific performance of copper and gold, both of which experienced all-time highs in 2024. For silver to achieve the same, it would need to exceed $50/ounce and therein lies my bullish thesis.

That said, I have adhered to my longstanding view that gold and copper will be the dominant metals in this decade and have avoided recommending silver or any of the silver stocks, including the juniors, and up until now, that has been the correct strategy. However, to coin a phrase popularized by John Meynard Keynes, "When conditions change, I change," and conditions for silver and the silver producers and developers appear to have changed.

Now, I am not going to go all "silver-buggy" in this missive because I still need to see silver hold this break-out level of $33.50 basis December. If we get a follow-through on Sunday evening when the access market opens, followed by the same on Monday when the COMEX opens, I will be taking a position in the iShares Silver Trust ETF (SLV:NYSE) along with some call options for leverage. There is a distinct possibility that we could see $37 and then $45, which sets up a decent trade in the near term. The break-out in silver, if it is real, further validates the bullish narrative for gold because, as you have all heard from me over the years ad nauseum, "no real bull market in gold can survive without the outperformance of silver."

Juniors

One of my favorite juniors is Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB) that last week announced the closing of a CA$2,121,733 financing, bringing their total 2024 funding levels to over CA$5 million, an outstanding accomplishment in what has been a difficult funding environment for the juniors.

I have known Chairman Campbell Smyth for over 20 years and consider him to be one of the savviest operators in the business and one helluva chess player. He has moved the Fitzroy pieces around the board like a bona fide Grandmaster resulting in a superb property package consisting of two Chilean copper-gold projects and one Argentinian (grassroots) gold project with drill programs expected to commence in 2024.

Also in the mix and high on their list of priorities is a "letter of exclusivity" signed between Fitzroy and a Chilean entity called Ptolemy Mining Ltd. that owns 100% of the Buen Retiro copper-gold project that is believed to carry the potential for a large-scale IOCG (iron-oxide-copper-gold) deposit comparable to the Candelaria Mine operated some 45 km away by the Lundin Mining Group. The company is awaiting exchange approval, so technically, they have not yet entered into an earn-in agreement, but it is this author's opinion that the deal will be consummated quickly, leading to an immediate drill program designed to confirm the existence of the IOCG mineralization.

Based on the geophysics, if the anomaly carries grade and scale and is indeed an IOCG, it is going to draw a great deal of attention from everybody including the majors in the region. This project (Buen Retiro) is a potential company-maker (and life-changer).

There is a vast array of junior developers and advanced exploration stories out there that are trading at "shell pricing" levels. In other words, their assets are being given little or no value relative to the market cap. This is where the incredible opportunities lie and where, in past cycles, fortunes were made. In the 1980's and 1990's, investors had to contend with flat metal prices for most of two decades relying solely on exploration success to advance valuations. In the 1970s, however, gold rose from $35/ounce to over $850/ounce, and that spurred massive investor interest in the junior miners.

Here in 2024, investors are blessed with record metal prices for gold and copper, but most other metals are still lagging, with the producers lagging even more. It is my opinion that junior developers with a defined resource are going to have outsized moves between now and year-end continuing on in 2025 with robust performances driven primarily, but not solely, by rising metals prices.

Also ripe for consideration is what happens when stocks top out, and trillions of dollars, yen, euros, and yuan all begin to compete for positions in the commodities sector, where the entire available supply of producers could be absorbed by one single fund alone.

A scary thought in the best of times. . .

| Want to be the first to know about interesting Gold, Critical Metals, Base Metals and Silver investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Fitzroy Minerals Inc.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Fitzroy Minerals Inc. My company has a financial relationship with Fitzroy Minerals Inc. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.